I have a confession to make: despite advocating for the importance of doing due diligence on a stock before clicking the buy button, I went against my advice and bought a listed company in Malaysia without doing any research. The stock turned sour. The company is Serba Dinamik, ticker symbol: SERBADK.

I invested into this company with the ang pow money from Malaysian relatives. Not to blame myself for having roots in Malaysia, but if I had not had Malaysian currency in the first place, I would not have invested in this company. How have I decided to buy into this company? I quickly skimmed through some analyst reports and suggestions from the broker and went ahead because it was only a small sum of money.

Just less than a month ago, when the company announced that KPMG refused to sign off its accounts, the news made headlines in The Edge Magazine, and was also reported in Singapore’s Straits Times and ChannelNewsAsia. That was when it caught my interest to delve into its financial statements. As the devil is in the details, I dug into the past years’ financial numbers and identified many potential warning signs. In hindsight, I could have avoided this stock if I had done my homework.

Here’s my findings. However, hindsight is 20/20 – here’s what I would have seen with perfect vision.

1. Unable to ascertain the legitimacy of certain trade receivables balances

In accrual accounting, once a service or product is delivered, the transaction will be realized as revenue, even if the cash is not received. Having a ballooning accounts receivable signals that the company is having trouble getting paid for its products or services. Look at Days Sales Outstanding (DSO).

DSO shows how many days it takes for a customer to convert account receivables to cash. This alone does not signal accounting fraud, but coupled with the fact that KPMG had difficulty verifying its clients and sales transactions did cause me to raise my eyebrow. The bulk of its account receivables originated from its customers in the Middle East, and KPMG had discovered that certain customers do not bear registration numbers – an ominous prelude to what could later become financial shenanigans.

There were many users in online forums who lambasted KPMG’s delay in sounding alarm bells after auditing Serba Dinamik’s accounts for many years. However, the situation is far more nuanced than it seems. If KPMG had discovered only one or two minor errors from past audits, I believe the auditor could let it pass. But, recognizing the growing trend of a poor earnings quality coupled with the difficulty in verifying sales transactions definitely raises some eyebrows, leading the auditors to scrutinize the accounts more closely this time round.

When it comes to trade payables, one of the findings by KPMG was that the fax contact number of its supplier (per the official website) belongs to one of the group’s employees using a ‘Truecaller’ Application. When a company’s supplier shares the same phone number as its employee, that gets me wondering: is there something behind the numbers? As an outside investor, I can’t be sure if the transaction is really at arm’s length between local suppliers and Serba Dinamik.

2. Consistent Gross Profit Margin (GPM), Operating Profit Margin (OPM) and Net Profit Margin (NPM)

The above is the GPM, OPM and NPM of the companies operating in the same sector as Seba Dinamik: Bumi Armada Berhad, Yinson Holdings Berhad and Wah Seong. Notice what they have in common: from the charts above, one should easily infer that the profit margins are quite lumpy but genuine due to the timing of contracts delivered.

However, the same cannot be said for Serba Dinamik, where its GPM and NPM have been very stable over the past five years. In my view, it seems too good to be true.

Moreover, 2020 was a challenging year for the Oil and Gas (O&G) industry due to declining oil prices, thanks to Covid-19. One does not need to look too far: Singapore blue chip companies like Keppel Corp and Sembawang Marine Corporation were struggling last year and their numbers are still in the red. Yet, Serba Dinamik miraculously defied all odds and managed to achieve an all-time high revenue and profit through inflating receivables.

3. Proposed to replace KPMG when audit issues were raised.

To add fuel to fire, just a few days after the financial report, the director proposed to replace its auditor from big four KPMG to BDO PLT. As the saying goes: Quis custodiet Ipsos custodes – who watches the watchmen? The watchmen are auditors and CFOs. To fire the auditor after some potentially damaging accounting issue surfaced is a major red flag to look out for; hence, I choose to err on the side of caution and cut my losses.

The board’s decision to persuade KPMG to resign suggested that management may have cooked the books and have something to hide. The market reacted to the news by sending the stock price tumbling. Even the reputable Employees Provident Fund (EPF) and Permodalan Nasional Berhad (PNB), who have been known for delivering promising returns, expressed their concerns. When the market opened on the June first, I tried to place a sell order below the last traded price to get my order filled immediately. I was dealt a shocking blow when I found out that I could only sell at a fixed price of RM 0.795. In the end I got my 1,200 shares filled at RM0.795 and another half at RM0.90.

Although the management gave in to shareholders’ pressure and shelved his plans on changing auditors, the damage had already been done and stocks showed no signs of recovery. Although the stock price reversed its course and shot up to RM0.75 (intraday gain of 24.8%) due to the news that Ernst & Young was appointed as an independent reviewer, it was short-lived and the stock gave up most of its gains in a short span of time.

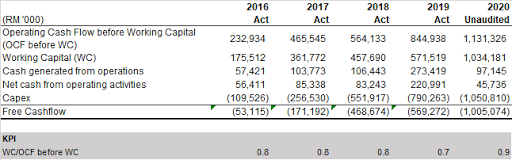

4. Consistently Negative Change in Working Capital

This is not accounting fraud, but it is a tell-tale sign of a company with poor fundamentals. When you have a negative change in working capital, it means that the company is investing heavily in its current assets and reducing its current liabilities. In Serba Dinamik’s case, its current working capital is made up of inventories, receivables, payables, and net contract assets. Hence, this suggests that Serba Dinamik is investing in most of its operating cash flow to ramp up on receivables and inventories. By doing a ratio between change in working capital and cash generated from operations before working capital, we get a ratio hovering close to one. That explains why there has been no free cash flow over the years. Most of their current cash, past dividends and capital expenditure were financed through issuance of term loans, private placements and proceeds from Sukkuk.

|

| Negative Free Cashflow for the past 5 years (RM ‘000) |

In a healthy financial statement, an increase in company cash flow from operations should track its increases in net income, and this divergence in number suggests that the company is generating sales without collecting the cash – in this case, on receivables and inventory. That probably explains why the auditor was concerned about its suppliers.

Once bitten, twice shy. It is indeed a sobering reminder for me to do my research on any stocks that I plan to buy, no matter how small the investment may be. But retrospectively, it is a blessing in disguise as the ‘school fee’ from my losses in this share is worth paying, since I have gained much insight on what’s ‘really’ behind the numbers.

Thank you so much for spending time to read my blog and I really appreciate you. If you enjoyed reading my blog, hope you can support me by liking my Facebook page here or share my post. Currently, I do not earn any fees through any affiliate programme or sponsor. If you have any queries, feel free to post them and I am happy to take questions! 🙂

I have learnt more about researching and analyzing a company from your posts than all the other articles put together. Thank you for making it easy to understand.

Hey KAM, sorry for the late reply. Thanks for visiting my blog and glad that you have learnt something!