invest in the STI ETF given the current levels hovering between 3.4k to 3.5k levels

and if yes, how to ride on it.

their daily emails to get investing ideas for past few years. Last week I

received an article by David Kuo that the total returns on Singapore market outperformed the Dow Jones Industrial average. Kinda surprised right? Me too!!!

In the last 12 months, our Straits Times Index has risen

around 8%. The Dow Jones Industrial Index has also gone up by 8%.

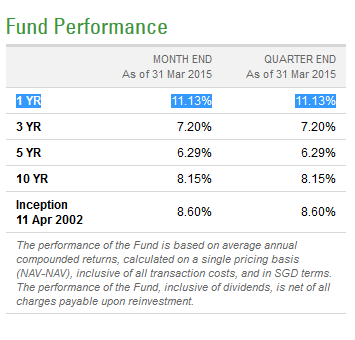

But when dividends are considered, the total return of 11.1% from our top

30 companies trumps the 10.6% return by America’s top 30 corporations.

but this is the closest I can find. (shown below).

purposes as of 31st March 2015:

All of us knew that Dow Jones had a good run last year, but

interestingly STI managed to outperform DJIA marginally by 1%. Also if one had

bought and hold for 10 years, he/she could have gotten returns of 8.15% per

annum and also outperformed the US market too!! Definitely more than enough to

beat inflation! Honestly, I doubt many investors can beat this return for a

year, let alone 10 years.

performance of Singapore shares, and with the low trading volume in STI suggests

lack of interest by institutions….but as long as one has the holding power, I

believe he/she is able to generate good returns in the long run. STI consists of

blue chip companies that generally pays more dividends that DJIA annually.

definitely trading at a cheaper valuation. (For Singaporean investors, do take

note that there’s a 30% withholding tax when one buys DJIA ETF in US Market).

So for every $100 of dividends declared, you will only be receiving $70.

|

|

STI ETF

|

DJIA ETF

|

|

PE Ratio

|

13.96

|

16.22

|

|

Dividend Yield (%)

|

2.65

|

2.04

|

|

P/b Ratio

|

1.35

|

3.18

|

It’s quite clear that STI ETF is cheaper.

see what the legendary investor, Warren Buffett has to say.

My advice to the trustee couldn’t be more

simple: Put 10% of the cash in short-term government bonds and 90% in a very

low-cost S&P 500 index fund. (I suggest Vanguard’s.) I

believe the trust’s long-term results from this policy will be superior to

those attained by most investors — whether pension funds, institutions or

individuals — who employ high-fee managers.

Here’s the link

either buy individual stocks, mutual funds or ETFs. In this post I ll cover more about ETFs.

2. SPDR STI ETF vs Nikko AM STI ETF

like the way you buy shares.

you invest in the fund. It tells you the return over different periods, the

shares that they are holding, net asset value (NAV), expense ratio and etc. Buying a

fund without reading the factsheet is like purchasing a house in Singapore

without knowing its location.

|

|

Nikko AM

|

SPDR

|

STI

|

|

Expense Ratio

|

0.42%

|

0.30%

|

–

|

|

1 Year returns (%)

|

10.98

|

11.13

|

11.57

|

|

3 Year returns (%)

|

7.31

|

7.2

|

7.87

|

|

5 Years returns (%)

|

6.15

|

6.29

|

6.78

|

the company. The percentage is obtained through dividing the fund’s operating

expenses by the average value of managed assets. A fund with lower expense

ratio is generally better.

there’s no point in doing so. Investing in index should be for the long term as

we can’t predict market’s direction in the short term.

and 5 Year returns by shy by 11 basis points for a 3 year returns. As a long

term investor, I personally prefer SPDR STI ETF, because of their better long returns and lower expense ratio.

Here it is!

|

1.

Stock Market (CDP) |

|

2.

Stock Market (custodian) |

|

3.

POSB Invest Saver |

|

4.

OCBC Blue Chip Investor Plan |

|

5.

Philips Share Builders Plan |

peach color uses dollar cost averaging whereas for the first and second option

is buying based on the amount of shares. No. 2 is highlighted in purple

(mixture of blue and peach) as the brokerage fee is low enough to sort of buy

100 shares monthly to match up the returns from dollar costs averaging. Although it’s not really buying with the same amount of dollars every month, but it can function like an element of dollar cost averaging

1. The first way is pretty simple. Just open a

brokerage account with a stock brokerage firm. Motley Fool even have a page to

list out all the firms and their commission fees. Check it out here. You can buy in lots. (1 lot=100 shares) but do take note of the fix commission

charges.

Standard Charted Online Trading. The commission is pretty low, at 0.2%. You can

consider buying 100-200 shares every month to sort of match-up with dollar costs

averaging. You can’t exactly call it dollar costs averaging because we are not using the same amount to invest every month, its more on the same amount of

shares in this case.

to invest less than $500 monthly. The commission charges is 1% so every $100

you put in $99 goes invested. You’ll be investing in Nikko Am STI ETF. The

shares will be under custodian with POSB

higher. So if you have $500 to set aside every month, this would be an ideal

plan to do dollar costs averaging. You will be investing in Nikko Am STI ETF,

and there are also about 19 blue chips shares to DCA from.

you’ll be buying SPDR STI ETF if you go with Philips. With this plan, you can

even reinvest your dividends for a fee.

|

|

POSB

|

OCBC

|

POEMS

|

|

Minimum Monthly Investment

|

$100

|

||

|

ETF

|

Nikko

AM STI ETF/ABF Singapore Bond Index Fund |

Nikko

AM STI ETF |

SPDR

STI ETF |

|

Shares

|

–

|

18 Blue Chip Counters

|

19

Counters |

|

Fees

|

1%

|

$5

or 0.3% whichever is higher |

Investment

of <$1000 |

|

$6 for ≤2 counters, and $10 for ≥ 3

counters. |

|||

|

Investment

of ≥$1000 |

|||

|

higher

of 0.2% or $10 |

|||

|

Dividends

|

Credited

to bank Account |

OCBC

Deposit Account |

Reinvestment

Option/ Cash on Request |

|

Recommended Minimum Monthly Investment

|

$100-$500

|

$500-$600

|

$600 and above

|

year to kind of set an example to my friends and show them it’s really the most

idiot-proof way to getting good returns. All I do is just to ensure sufficient

funds for GIRO to go through to buy the funds every month.

Chartered. I started with Nikko then because they can be bought in 100 shares. With

the reduced lot size from 1000 to 100 this year, I have switched to SPDR.

dividends and capital gains yield e.g First Reit, SATS etc., STI ETF will

always have a place in my portfolio. So to all busy people who have no time to

monitor the market or do any sort of fundamental analysis, this is for you.

4. Some Interesting Facts about Nikko AM STI ETF

1. In the past Nikko AM STI ETF does not hold actual shares of the bluechips to mimic the index performance, but uses derivatives and swaps to track the index movement, hence exposing itself to counter party risks

In the end of April, it appeared to have changed its investment focus so it “will not use or invest in financial derivative instruments”

any longer in its aim to mimic the STI’s returns. So it is now holding the STI’s 30 shares in the

appropriate proportions.

Distributions, if any, will be determined by the Manager. Currently, it

is the Manager’s intention to make distributions to Holders

semi-annually around January and July of each year.

The Manager will decide whether a distribution is to be made based on

various factors, including dividend and/or interest income and/or

capital gains derived from the investments of the Fund. Distributions

will only be paid to the extent that they are covered by income received

from underlying investments of the Fund and are available for

distribution.

Nikko AM STI ETF shareholders only enjoyed one distribution last year and earlier this January whereas SPDR enjoyed two payouts last year. That probably explains the difference in prices.

5. References and useful links

On STI ETFs

http://www.fool.sg/2013/10/18/straits-times-index-etfs-made-easy/

http://www.fool.sg/2013/03/30/making-etfs-safer/

About Nikko Amended Distribution Dates

http://www.turtleinvestor.net/nikko-sti-etf-amended-dividend-distribution-dates/

Importance of Dollar cost averaging via Index

http://www.fool.sg/2013/10/08/what-do-regular-shares-savings-plans-mean-for-your-financial-future/

http://www.fool.sg/2014/03/25/straits-times-index-etf-generated-8-4-annualised-returns-over-past-10-years/

Methods to buy the index

http://blog.moneysmart.sg/invest/posb-invest-saver-ocbc-blue-chip-investment-plan-poems-share-builders-plan-which-regular-savings-plan-to-use/

http://www.bigfatpurse.com/2013/11/sti-etf-monthly-investment-plans-comparison-why-poems-share-builder-plan-is-preferred/

Thanks for reading! and thanks again for your patience. I am not really a good writer as I have struggled with languages since Primary One and even till now…Nevertheless, I ll find ways to improve my English and my language expression. I believe life is all about learning and benefiting the society.

Anyway, if what I have shared benefited you, do support me by liking my Facebook page here or you can just click the ‘like’ button on the top right hand corner of this page.

Do drop me a feedback/comment on areas which I can improve on or stocks which you would like me to cover.

God Bless!

Hey EotS,

Excellent post! The SPDR also has deeper volumes, which is pretty important if you want to fill your full order at a given price.

I saw that you mentioned DCA quite a bit. Have you ever thought about Value Averaging (VA) as an alternative method to deploy capital on a regular basis?

Hi flyfox, I also have a portion of my investment portfolio as an STI ETF (Nikko am before 100shares = 1 lot).

I've been pondering on this question, whether to go all in STI ETF with bonds for my portfolio or to have a split between active stock picking and STI ETF and bonds, something like a core-satellite approach, but without the mutual funds.

My main problem is that, index investing should be fine in the long run, but I can't help but to pick certain stocks that I like. However, in the long run, wouldnt this affect my portfolio performance? Given that mutual funds are proven to statistically underperform index ETFs, picking individual stocks kind of mimics this issue.

Therefore am I setting myself up for failure (By this, i mean less then market returns i.e. from indexing) by doing a half-half approach? I have no correct answer / it's grey area to me. Would like to hear your views 🙂

Out of curiousity, do you rebalance your portfolio between active stocks and sti etfs? What % portion of ur portfolio do you have in sti etfs vs individual counters? Wondering on what number to go for my personal portfolio.

Cheers! Great concise write up btw, shared 🙂

Hi EOTS,

Rather than STI ETF, I would recommend SSE ETF.

China's bull market will keep outperform.

So, SSE ETF is good to buy.

Hi mmmhou,

Sure! Thanks for bringing this up 🙂

The closest ETF on SSE that I can find in SGX is UETF SSE50China (JK8). The YTD returns is a whopping +35.48% and a 5 Yr return is +7.90%. Or you can buy from other stock exchange but do note on their dividend withholding tax rate.

Also their price to earnings multiple is abit on the high side though..

However, i am not too sure if you can do dollar costs averaging for it. Or one method is to use StanChart to buy 1 lot/month to save on brokerage fees in the long term.

When we do DCA our investing horizon should be for the long term. In fact short/medium term bearishness works well as we get more buy more units at the same costs.

http://www.bloomberg.com/quote/USSE50:SP

https://uniservices1.uobgroup.com/secure/forms/china_etf.jsp

http://davidstockmanscontracorner.com/shanghai-composite-pe-ratio-reaches-44x-the-price-to-whatever-bubble/

Hi GMGH!

Thanks for sharing with me the idea of Value Averaging. Honestly, it's really something new to me.

I just read this concept online: http://www.investopedia.com/terms/v/value_averaging.asp

Will read up more and consider this method.

And I agree that SPDR has deeper volumes, easier to get our orders filled. Thanks for bringing it out 🙂 Will update it in my next post 🙂

That's what's blogging all about, learning from each other.

Hi JD!

Sorry for the late reply and thanks for sharing and appreciating my write-up. It means a lot to me who struggles with writing. 🙂

There’s nothing wrong with picking stocks even there could be times we lose to market returns. What I suggest is to always have a portion of STI ETFs in your portfolio for long term. The percentage will depend on how active you are in your investment.

Also I don’t think it’s wise to compare stocks and mutual funds. For the former you do your own homework so you don’t pay fund management fees and not subjected to higher bid offer spread. Sometimes fund managers are also bound by the sectors they can invest in and they can’t simply switch to hold all cash so when market is toppish. However I am not against unit trusts as there are funds run by some asset management firms which outperform the market . I like Aberdeen in particular. 🙂

I have yet to do any rebalancing but moving forward I might take a more passive approach in investing so probably will have ETF take up 20% of my portfolio. I wont sell my stocks for the switch but I ll buy more ETF I guess. Currently ETF takes up about 10% of my portfolio if I were to include my those under custodian with StanChart and POSB

Hope all the above answers your question. 🙂

Hi EOTS.

Great post on the summary of STI ETF. Can you kindly point out where do you find the disallowed partial redemption for the POSB invest saver and Blue Chip Investor Plan? The nearest related point that I can find for OCBC is on point 14 of the FAQ which seems to contradict with yours. It will be a pity that both plans do not allow partial redemption of units.

http://www.ocbc.com.sg/personal-banking/Investments/bcip-faqs.pdf

kh

Dear Anonymous,

Thanks for bringing this out!

Apparently I read from these links:

http://www.bigfatpurse.com/2013/11/sti-etf-monthly-investment-plans-comparison-why-poems-share-builder-plan-is-preferred/

http://madstranger.blogspot.sg/2013/07/posb-invest-saver.html

https://thelesstraveledpath.wordpress.com/2014/06/25/review-of-posb-investsaver/

that no partial redemption is allowed for POSB Invest Saver, but I went to look further after you brought this up : http://gotmoneygothoney.blogspot.sg/2014/09/posb-invest-saver-20-new-and-improved.html

and https://www.posb.com.sg/personal/investments/trading-funds/invest-saver

Under Step 4: Input the number of units to redeem and select the account to credit your redemption proceeds.

and it looks like POSB now allows partial redemption.

I guess the OCBC part was my mistake too. Sorry about it. Will do the amendment asap!

Seems like all 3 allow us to sell odd lots. 🙂

hi thanks for the informative post! may i ask with regards to the purchase of the STI ETF for example through POEMS, which you mentioned that I'll be buying SPDR STI ETF, would I be able to purchase all the top 30 stocks with a RSP? because their website mentions that i can "choose" from a list of 19 counters.

From my understanding, how the ETFs work here is that a fund manager will actively replace the 30th top performing stock, hence Neptunes Orient (NOL) is out of the top 30 and replaced with another stock. But I don't understand how we would make use of this if we were to invest in a RSP through OCBC, POSB or POEMS, since we have to choose how much to invest for each "counter" (which is 18 or 19 for POSB and POEMS).

i.e let's say with $100, is it possible to allocate the amount for each of the 30 top performing stocks?

STI ETF is definitely the way to invest over a long term to reap its benefits. The only question is whether to go for POSB or SCB depending on individual risk preference.

Hi… I would like to understand if, for investments with posb invest saver. is the recommended $500 like $500 for ABF and $500 for Nikko? Or $500 for both add up (eg 200 for abf, 300 for nikko)?

Hi,

Sorry for the late reply.

The reason why I posted $100-$500 for POSB Invest Saver is because within this range, 1% sales charge is the best you can get (Nikko STI ETF), and 0.5% for (ABF). i.e Poems is charging a min of $6.41 (w GST) hence, for $500 investment charges for POEMS are:

$6.41/($500-$6.41)*100%= 1.3% or

simply 6.41/500 *100%= 1.28% >1%

for POSB Invest Saver

1.$200 ABF +$300 Nikko

($3+$1)/($500-$3-$1)*100%= 0.807%

2. $500 for Nikko

($5)/($500-$495)*100%= 1.01%

Hence,it's recommended to go with Posb Invest Saver (be it $500 or both add up)

Hope it helps!

-EoTS