September has been a month of correction for US market, with tech companies taking the hardest hit. Market darlings like Apple, Zoom & Tesla retreated from their all time

high and I took the opportunity to take a bite at Apple stock. With the upcoming US presidential Election and the growing Covid 19

numbers, stock market might stay volatile till end of the year.

While many beneficiaries of Covid

19 companies are still trading at very high valuation, I have to be more selective of companies to invest in. One of the shares which I believe is reasonably trading below its intrinsic value is JD.com.

I bought 50 shares of JD in 2018 at the price of $37 and

$41.40 when it was not profitable back them. When Liu Qiangdong was

investigated on the suspicion of rape, I then added another 20 shares at $27.50. The stock price hit rock bottom at $19.27 before it recovers. I am glad that I hold on to the shares as I believe the JD has a good business model will get through this. Moreover, he was not convicted of the crime, but only accused.

In August, I added 10 more shares at $75 and $78.8 after it

reported a solid set of results. It then rallied to $80 and closed at $76.10 last Friday. Despite YTD return of 113.45%, I believe there’s more room to

grow.

Diversifying their earnings with warehousing and fulfilment

centres

JD , also known as JingDong, is a B2C ecommerce company

founded by Liu Qiangdong and named after him and his ex girlfriend Gong

Xiaojing. It is also known as the Amazon of China, as it builds and invests in

its own logistics and delivery network through it’s own business group known as

JD logistics. While investing in its own logistics network comes at the cost of

its operating margin, it is an important part of its long-term strategy to digitalize

the logistic system to manage their supply chain more efficiently. Since logistics is a business built on scale, so as they continue to grow in scale and orders, their

margin should trend better. This can be evidently seen during the Covid

19 times, where delivery costs go to all time low due to increased order volume

caused by the pandemic and costs controls. Check it out here

Also, having in house fulfilment means that they could have

better control over the costs in the long run through and won’t be at the mercy

of third-party logistics to set delivery price or impose price hike. Other than

benefitting from economies of scale, they are also leveraging on 5G as well as

its big data resources to build an efficient logistic system which could

further lower operating costs for the long term. Just last year, it recently

launched 5G-powered smart logistic park in Beijing which aims to tap into the bandwidth

offered by 5G to increase its operating efficiency of JD’s Industrial Internet

of Things (IIOT) fulfilment operations as well as better interaction between

employees and smart machines.

JD, being a much smaller company relative to Amazon, has

higher fulfilment capacity-730 warehouses (183mil square feet) compared to

Amazon’s 175 ($150 million square feet). They have even formed a logistic

network with the ability to fulfil 90% of direct sales in 24 hours. Hence, JD

has much capacity to support its growth in sales with its current warehouse

footprint. With that excess capacity, JD could offer its service to 3rd

party companies to drive revenue growth. For instance, Just ten days ago, Aiqin, China’s leading maternal

& infant chain store announced a partnership to outsource it’s fulfilment

to JD Logistics. According to Aiqin, the number of defective goods delivered to

store has reduced to lower than 7% after switching to JD logistics.

Below is JD’s Gross Profit and & Operating Margin

It’s evident its gross & operating margin has improved

over the years and the trend suggest that it will continue to improve as

logistics business get more profitable. JD logistics was spun off in 2017 to

a separate business unit, and with many institutional investors such Tencent and Sequoia Capital as its shareholder , I believe it’s a matter of time JD Logistics will be listed in the

stock exchange. https://www.bloomberg.com/news/articles/2019-12-23/jd-logistics-eyes-ipo-to-raise-up-to-10-billion-reuters-says

What this means is that will translate to higher operating

margin and hence higher profitability, as logistics will not weigh into the

cost of revenue and operating costs once listed. Moreover, shareholders of JD could

potentially enjoy a special dividend or given shares of JD Logistics.

JD Cloud

Another way of improving its operating margin is through its cloud services. In 2019, JD announced a partnership with Cloudflare to

strengthen its cloud and AI business. Currently it’s revenue stream is too

small to move the needle in its total sales growth, but in the long term it

is expected to form a new recurring income steam for its cloud and AI business

with cloudfare paying JD to use its data centres. It’s margins may not be as

impressive as AWS but sure it will go beyond its current operating margins of 2.17%.

In China, Alibaba is the leading cloud player, followed by

Tencent & Baidu. Since the start, Alibaba’s cloud segment has been in a

loss-making stage as they focused on growing

their market shares. While doing so, it managed to narrow its loss with time. Just a few days ago, CFO of Alibaba came out with the news that

its cloud computing segment is expected profitable in 2021, sending shares up

6.16% on Nasdaq (30th Sept). This suggest that it could take a few

years for JD Cloud to be profitable and with evolving technologies like AI and

Internet of Things (IOT), cloud service will continue to be in demand and

highly profitable.

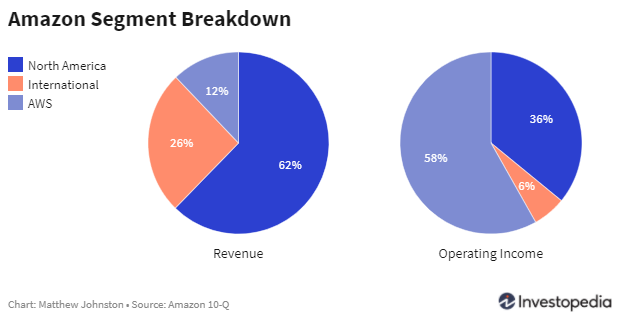

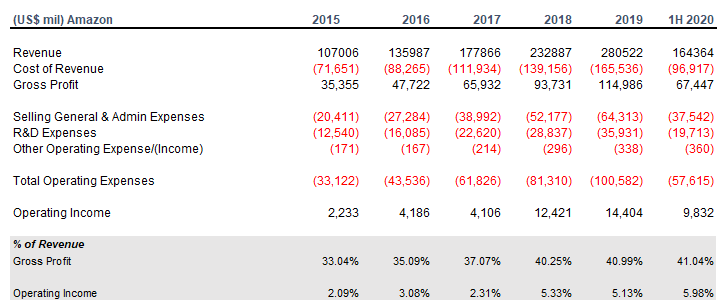

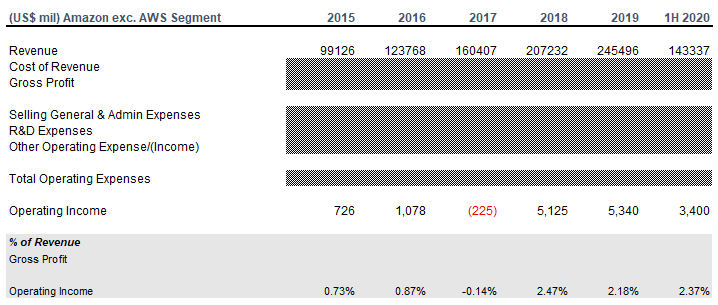

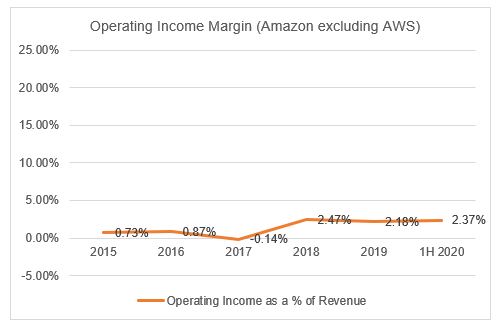

In the case of Amazon, just look at the chart below on how

much AWS makes a difference in its operating profit.

Amazons’ revenue stream comes from 3 segments: North America, International and AWS.

AWS made up only 12% of revenue but contributed 58% of total operating income.

The latest report shown an operating income margin of 5.98%, however without AWS its profit margin only come in at 2.37%.

|

Valuation

Presently, at the price of $76.10, and with current FCF (TTM) of USD 3.217 Bil and 1.56 Bil shares outstanding, it is trading at Free Cashflow Multiple multiple of 36.9. In my opinion, it is cheaply valued, considering that not many companies with potential growth of 39% y-o-y (see below) is trading at 36.9x FCF. Its closest peer I can think of is Amazon and it is trading at P/FCF of 58.

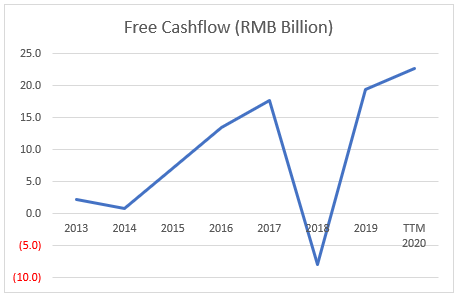

Below is the JD’s FCF since 2013. Its cashflow has generally been on an uptrend with the exception of 2018. The 2Q 2020 report highlighted that it was a one off due to decrease in advance payments from customers for their marketplace.

|

| Year on Year Growth (2013-2019) is 39.7% |

Historically its FCF was growing

39% (2013-2019) and with possible listing of JD logistics, its capital

expenditure could be significantly reduced and hence a higher FCF. Also, JD

cloud is still in its early days and could generate

stable cashflow for JD once it turns profitable like Alibaba Cloud.

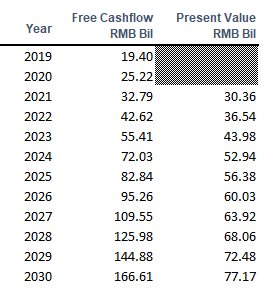

To calculate present value, I

would assign a discount factor of 8%, with a growth rate of 30% (Year 1 to Year 5), 15% (Year 6 to year 10) and 5% (Year 10

to 15).

Sum of PV of Cashflows= 1014.96 Bil

RMB.

Total shares outstanding= 1.56 Bil

Present Value (RMB) = 650.6154

1USD: 6.79 RMB

Present Value (USD) =USD 95.82

Potential Upside = 25.9%

What are your thoughts on JD? Do you see its potential in the long term? If yes, will you consider adding at current levels?

Thanks for checking out my posts. If you are keen to follow my posts or get updates, do like/follow my FB page here where I will update it when there’s a new post.