Fiverr is an Israeli online marketplace which connects

freelancers with buyers. It was founded in 2010 by Micha Kaufman who is also

the current CEO and claimed to have started the concept of Service as a Product

by offering digital services in exchange for a small fee. The popular service

that was offered during its earlier days was Logo design for $5 and hence its

name, Fiverr. The platform began to grow as more services are being offered, bringing

freelancers from offline to online and digitizing their services.

For instance, if a buyer wishes to source for a gig worker

to design his website, he can pick the ideal freelancer by reading reviews, pricing, asking a few questions. If the end-product is not

satisfactory, the online gig could either raise a dispute or cancel the order

and funds will be reimbursed to the buyer’s account.

Back then, I was a customer of Fiverr before I invested in

this stock. I first got to know this company when I was looking for a

freelancer to optimize my LinkedIn profile and I must admit that I was spoilt

for choice when I was scrolling through the list of freelancers.

The experience was smooth and since then I have been regularly

using Fiverr. Also, I need not worry about freelancers failing to deliver the finished product or go missing as it is in the interest of the freelancers to make us feel

satisfied with the product so that they can receive positive reviews.

When I came to know this stock late last year, it has

already gone up 10X since its listing. In fact, you will be surprised that it

outperformed Tesla in term of 1 year return. Yet the 10X return make sense as

Covid-19 pandemic has increased motivation for business owners to work with

freelancers and working from home has encouraged full time workers to try out

freelancing. And Fiverr is one of the best platforms to start with, as it matches

the freelancer with the right buyers without the need to spend on marketing or

upfront meeting costs.

And the numbers in 3Q 2020 proved to be true with strong

revenue growth and smashing analyst expectations.

Despite going up 10x since it’s IPO price of $21, I believe

it has much more room to grow and I got in at average price of $ 241.

Here are a few reasons which I believe that the best for

Fiverr is yet to come!

1. Moving further upmarket

Fiverr Pro

Fiverr derives its Revenue using the formula: Active Buyer X Spend Per Buyer X Take rate. And

moving upmarket is to increase the spend per buyer and hence Fiverr pro was

introduced back in 2017. What sets the Pros apart from other freelancers is former

experience in working in big and influential brands and having unique field of

specialization. Generally, they attract big companies which require high end

professional work as well as working on milestone. For instance, a movie

production involves script writing, shooting each scene and video editing. Hence

with Fiverr Pro, global brands can hire a specific pro which specialize in each

milestone. If the Pro fails to meet the required standards, they can easily replace

with another Pro to complete the project without spending money on hiring costs

and dealing with regulatory compliance by hiring and firing.

Fiverr Business

Fiverr for Business was launched in the middle of the

pandemic to define the future of work. It is tailor made for business teams collaborating

on a project and needing to hire a freelancer. For instance, a group of

employees developing a new advertisement can head over to Fiverr Business

Platform to source for the right gigs and have a group chat functionality or

setting up a Zoom call to discuss on the progress. Imagine having tight

deadlines and having to submit your project the next morning. With Fiverr

Business, the team can outsource the job to freelancer in US and brief the

seller on the requirements and get the completed work the next morning.

Fiverr is offering first year free to capture the market

share but will be chargeable at $149 for annual subscription. With Fiverr

Business, HR need not screen through resumes and or conducting job interviews

to hire a part time staff to complete a project. All it takes is $149 and

Fiverr does the handpicking of the best talent who has what it takes to cater

to business audience and certain level of professionalism in the way they communicate

and getting work done.

2. International Expansion

|

|

Olá: Fiverr Announces a |

In the past few years, Fiverr has successfully expanded into

European markets and recently announced their expansion in geographic footprint

to Latin America countries. While Fiverr is already globally accessible,

international expansion means offering the possibility accepting local currency via local payment

methods and presenting in their own native language which in turn

increase take up rate and a better platform experience. For instance, to

capture the market in Brazil, Fiverr has successfully launched its service in

Potuguese (native language of Brazil) and start accepting Boleto and Reis (payment

method in Brazil). It paid off and Fiverr saw a 137% increase in freelancing

service from Brazil. The same can be said for Mexico, where Fiverr offered a

local language site and allows local payment in cash through partnership with Oxxo,

a leading convenience store chain. With that, Fiverr saw a 100% uptick in

Mexican freelancers joining the platform.

These shows Fiverr’s ability to scale to capture more market share to

strengthen its ecosystem of freelance service online.

3. Huge Total Addressable Market

There has been a trend towards gig economy and Covid 19 has only

helped to expand exponentially. As retrenchment is prevalent during pandemic

times, gig firms such as Grab Delivery or AirBnB helped to reduce the strain on

unemployment and put food on the table. While the pandemic will eventually disappear, I believe that the world has already embraced this new way of working.

Even those who found their full time job may be open to selling their

services on Fiverr after their work hours, and drivers would embrace hitch to

earn extra income on commuting. Perhaps Covid-19 is all it takes for many to

find out that full time employment may not be their cup of tea after all— it

lacks freedom, flexibility, and ownership. In general, millennials grown up in

a world shaped by technology and start-ups and they are more willing to

tolerate changes and uncertainty in their work. In exchange for job security,

they strive for some ownership in the work they do and the freedom to work

anywhere and anytime they want— by the beach facing the sun with their toes

are squishing on the sand or even in a café overlooking the winter scenery with

falling snowflakes.

|

| You can freelance anywhere with a laptop and internet connection Source: thriveglobal.com |

This translates to more companies adapting to this new way

of working and hiring workers. After all, it is more cost efficient than hiring

a full-time employee and they can save on taxes, worker compensations, applying

work permits and pay bonus. They also save on office space to

house hired employees.

One good example which gig economy is disrupting is the

healthcare sector. There has been growing interest in telemedicine, and thanks to

start-ups and app which allows anyone to connect to a physician at the comfort

of their home via video call and medication delivered to their home. I won’t be

surprised if Fiverr will onboard physicians to provide teleconsulting soon.

|

| Teleconsulting on the rise. Photo source: Business Times |

As more professions starts to embrace and participate in freelancing

service, I believe Fiverr will be in a position to capture more market share and

in the process to strengthen its moat becoming a central big force in the gig

economy.

Valuation of Fiverr

I will be using two step discounted free cash flow model to

determine the intrinsic value of Fiverr.

I will start with forecasting the Q4 earnings and project it’s free cash

flow and then combine with the past three-quarter results to get Full Year

earnings and FCF. The next step would be

to project the next 10 years financial results and perform the DCF to calculate

its per share value.

Step 1. Determine the net income of Fiverr

Management have provided guidance that Q4’s Revenue would be

in the range of $52.4 to $53.4 mil. Therefore, I will be take the higher end- $53.4mil.

I am not being unconservative here considering that

management always under promise and overdeliver the performance. In Q3 guidance, management projected $48-$49mil guidance after raising guidance

yet achieved $52.3mil.

Its gross profit (GAAP and non-GAAP) has increased over the

years which signals the higher potential for profit and I will use the same

gross profit margin (GAAP) of 83.3%. The same margin as Q3 will be used in deriving

the list of operating expenses.

|

| Improving Gross Profit Margin every year |

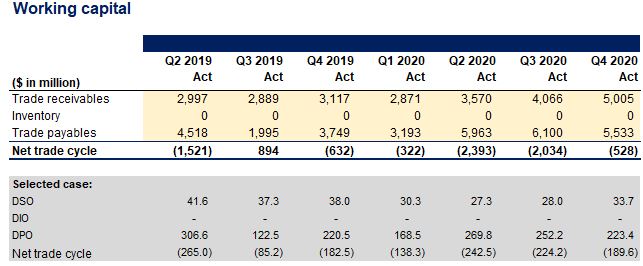

Step 2: Derive Trade Receivable and Trade Payable using an

average of DSO and DPO for the past 6 quarters.

Step 3: Determine

D&A and obtain Free Cash Flow for Q4 2020.

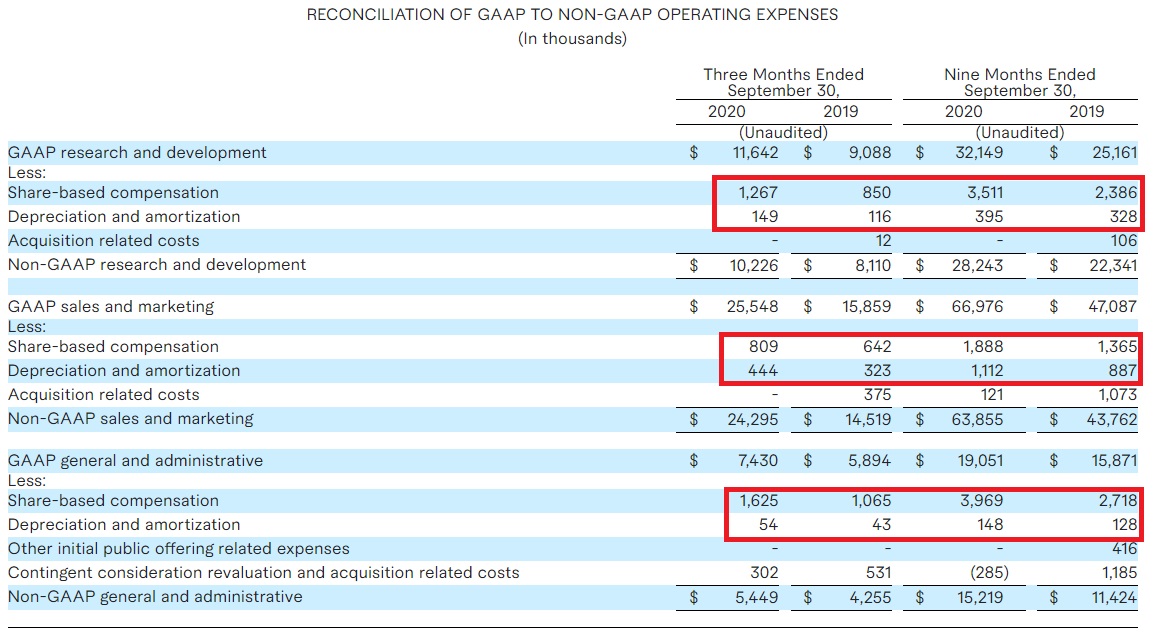

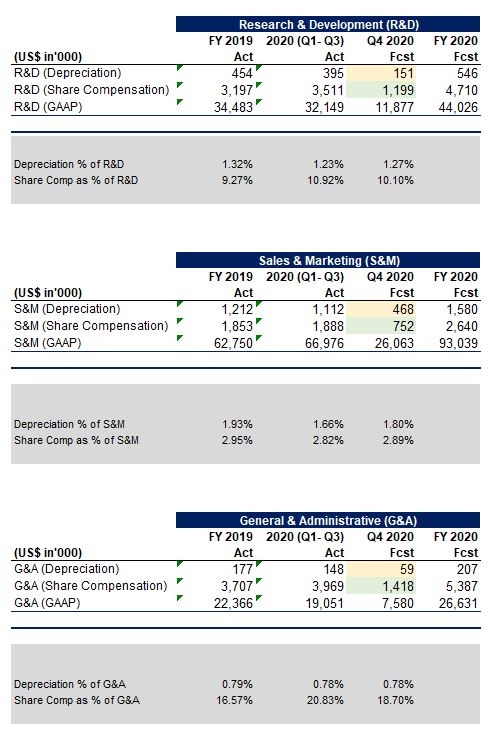

Depreciation and Amortization & Share Compensation

The D&A shown in Cashflow statement consists of:

D&A from Costs of Revenue + D&A from Operating Expenses

The same goes for Share Compensation

Share Compensation from Costs of Revenue + Share Compensation from Operating Expenses

D&A and Share Compensation from Operating Expenses

For D&A and share compensation from Operating Expenses,

management did a breakdown on the Operating expenses due to Depreciation and

share-based compensation (see above). The purpose is to show the GAAP vs Non-GAAP earnings

where non-GAAP does not take D&A and share compensation expenses to determine its EBITDA

margin. To determine D&A and Share compensation to be added back to

cashflow, I take the average of FY 2019 and 3Q 2020 Depreciation and share compensation as a % of the operating expenses.

Step 4. Work out the Cashflow for Q4 2020

Total D&A for Q4 2020= 587 (D&A and Share comp. from Costs of

Revenue i.e. 1.1% of Q4 2020 Revenue) +151+468+59

= USD 1,265,000

Non-GAAP Gross Margin= 84.4%

Gaap Gross Margin= 83.3%

Hence difference in Gross Margin= 1.1% of Revenue which

accounts for share based Compensation

US$53,400,000 *1.1% = US$ 587,400

Although the difference between GAAP and Non-GAAP consists

of Share compensation and D&A, I will lump under D&A for simplicity

sake.

User Funds

This consists of buyer prepayments inclusive of

company’s transaction fees which will be earned when once an order is

completed. User accounts would be funds which is transferred to seller’s

account upon delivery of the project. As the company doesn’t have the ownership

of the funds and they usually cancel off each other since payment is

transferred from buyer to seller eventually, I would not include it in my FCF

calculation.

Capex as a % of Revenue stays at 2% in past years. I will be excluding

business acquisition of ClearVoice, Inc, in Feb 2019 amounted to US$ 9.9mil,

since it is a onetime expense.

Step 5: Projecting future Net profit

Step 6: Determine Depreciation and Share Compensation as a %

of Operating Expenses for next 10 years and beyond

Step 7: Determine working Capital for the next 10 Years and beyond

Step 8: Calculate the Free Cash Flow

Summing up present value = US$3,031 which is 9.5X the

current price, almost a ten bagger. I believe there’s more upside to this stock

compared to Square, since the next 10 years of cashflow adds up to US$219, which

made up of 68% of current share price.

I am getting this blog post up ahead of earnings release in a few hours time and I can’t wait to see what’s in the cards as Fiverr reports Q4 earnings.

My Transactions

Thank you so much for spending time to

read my blog and I really appreciate you. If you enjoyed reading my blog, hope

you can support me by liking my Facebook page here or

share my post. Currently, I do not earn any fees through any affiliate

programme or sponsor. If you have any queries, feel free to post them and I am happy to take questions! 🙂

First time reading your blog. Really enjoyed the way you analysed Fiverr! Curious to know your thoughts after their latest earning release.

Wow,, P/S 86 and P/B 66, is this really under value???

peter

Hi,

Thank you so much for visiting my blog!

Their latest results are within expectations. Although results exceeded forecast but it is very normal since management had been setting low targets in the past.

Hi,

Thank you for visiting my blog.

I won't be too concerned about earnings in this case, as Fiverr spends much of it's revenue on operating expenses such as S&M and R&D to further scale its business and capture market share.

And yes, valuation look rich with p/s of 66 but I believe the gig economy is still in an infancy stage and has much to grow. The fact that it's trading at high valuation implies that market expects rapid growth. Even if the ratios looks high and stock looks expensive, it can ultimately be undervalued if Fiverr can exceed those demanding valuations.

Thanks for the really detailed analysis. I largely agree with your analysis and really like the detailed breakdown to get free cashflow. The revenue projection is very aggressive – in 10 years this company is projected to have ~100x revenue from today is what I'm seeing?

Would you be open to sharing the sheet so that I can play with some sensitivites on the projections?

Thank you so much for sharing this unique and wonderful post! There is useful information in your blog. There is a lot of knowledge in this. Our Fiverr clone app script is very easy to use and does not require much technical knowledge. Suffescom Solutions has a tendency to listen to the needs of our clients and ensure that your website reaches out to small job seekers and freelancers, which is important.