{kind=link}

UiPath’s stock has faced significant headwinds over the past year. Revenue growth has decelerated, concerns about AI disruption persist, and the share price has declined substantially from its peaks.

Despite these challenges, I believe the market may be underestimating UiPath’s strategic position in the emerging AI automation landscape. Here’s my analysis of what’s happening and why I’m maintaining conviction in this investment.

Understanding UiPath’s Business Model

UiPath provides enterprise automation software that helps companies automate repetitive digital tasks – things like data entry, invoice processing, and moving information between different systems. Their software robots (bots) perform these tasks automatically, improving efficiency and reducing errors.

UiPath generates revenue through three distinct channels:

1. License Revenue (~30-35% of total revenue)

Perpetual licenses for on-premise deployment, similar to traditional enterprise software sales. Customers pay upfront for a license key and deploy the software in their own infrastructure.

- Extremely high gross margins (~90%+) since it’s pure software

- Important for regulated industries (finance, healthcare, government) that require on-premise solutions

- Mature and stable, but not the primary growth driver

2. Subscription Revenue (~55-60% of total revenue)

Cloud-based Software-as-a-Service (SaaS) model with recurring annual or monthly subscriptions. This is similar to how Adobe moved from selling Photoshop boxes to Creative Cloud subscriptions.

- Strong margins (~80-85%)

- Recurring, predictable revenue stream

- This is management’s strategic focus – the shift from license to subscription mirrors successful transformations by Adobe, Microsoft, and others

3. Professional Services (~10-15% of total revenue)

Training, implementation support, and consulting services to help customers deploy and optimize their automation.

- Lower margins (~20-30%) due to labor costs

- Primarily serves to ensure customer success and drive adoption

- Not intended as a major profit center

Recent Performance Challenges

The stock has experienced significant pressure, and it’s important to understand the underlying factors:

Decelerating Revenue Growth

UiPath’s revenue growth has slowed from 30-40% annually to approximately 15-16%. While the company is still growing, the deceleration has concerned investors who prioritize growth momentum.

Net Revenue Retention Decline

Net Revenue Retention (NRR) – which measures whether existing customers are spending more year-over-year – has declined from a peak of 140%+ to approximately 107%.

The important context: This decline appears to be driven by market saturation rather than customer churn. Traditional RPA deployments have reached a natural ceiling within existing customer bases. Companies can only automate a certain percentage of processes with rule-based bots before reaching diminishing returns.

The gross retention rate remains healthy at ~98%, indicating customers are staying but not expanding their traditional RPA footprint.

AI Disruption Concerns

The market has questioned whether AI agents and large language models will make traditional RPA obsolete, potentially disrupting UiPath’s core business.

This is a legitimate concern that deserves careful analysis, which I’ll address in the next section.

What Remains Strong

Despite these headwinds, several fundamental metrics remain solid:

- Revenue continues to grow at 15-16% year-over-year

- The company achieved its first GAAP profitable quarter in Q3 FY2026

- Gross margins remain above 80%

- Strong balance sheet with minimal debt

- Generating $370M+ in adjusted free cash flow (FY2026 guidance)

- Market-leading position in enterprise RPA

- High customer retention (98% gross retention)

The business fundamentals suggest this is a transition period rather than structural decline.

The AI Opportunity: Expanding What Can Be Automated

Understanding UiPath’s strategic position requires looking at how AI agents differ from traditional RPA and why this matters for growth.

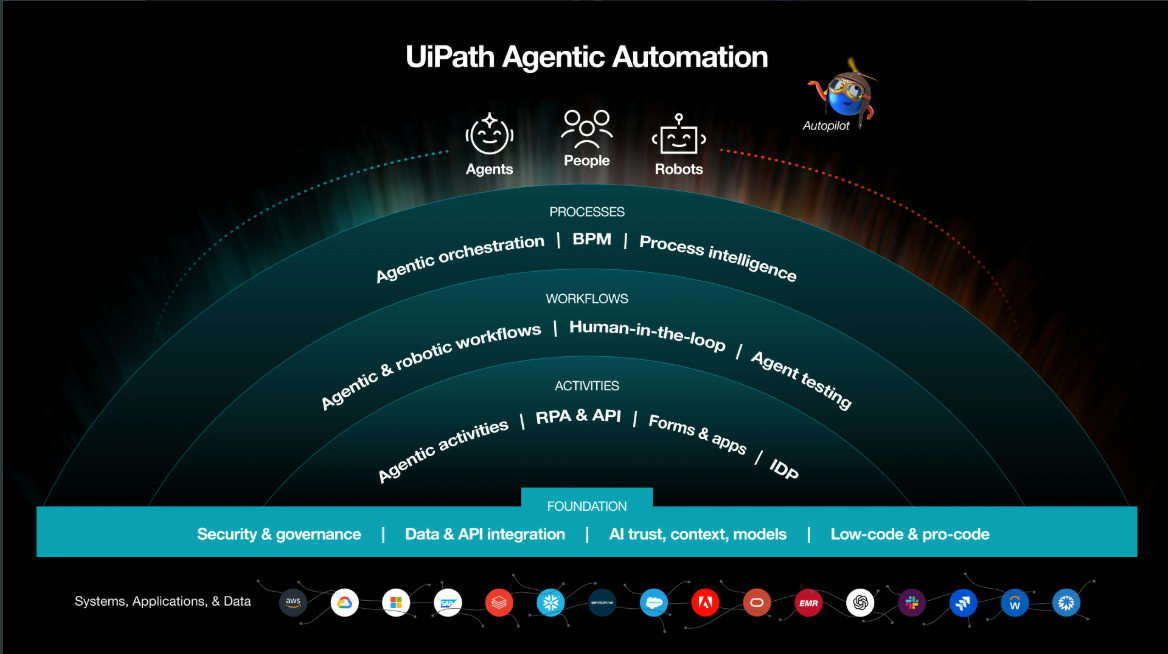

The Three-Layer Architecture

To understand where UiPath fits, think of AI automation in three layers:

Layer 1: Foundation Models – OpenAI, Anthropic, Google, Meta (the AI “brains”)

Layer 2: Applications – Microsoft Copilot, ChatGPT, Claude.ai (user-facing AI)

Layer 3: Orchestration – UiPath (coordinates multiple AI models, RPA bots, and human workflows across enterprise systems)

The key insight: UiPath doesn’t compete with OpenAI or Microsoft Copilot. It sits above them as the “conductor” that orchestrates different AI models, legacy automation, and human workflows into complete business processes.

Why Traditional RPA Hit a Ceiling

Traditional RPA excels at automating structured, repetitive processes with clear rules – things like data entry from standardized forms or moving information between fixed fields.

However, RPA struggles with unstructured data and judgment-based tasks – interpreting varied email formats, analyzing documents without standard layouts, or making contextual decisions.

The saturation issue: Companies automated their most repetitive processes first. Once those were done, the ROI on additional RPA deployments diminished. There’s only so much cost reduction you can achieve before hitting a natural limit.

How AI Agents Expand the Market

AI-powered automation addresses these limitations:

- Unstructured data processing – Can read varied document formats, emails, images

- Adaptive decision-making – Makes contextual decisions based on learned patterns (similar to how Tesla’s Full Self-Driving evolved from hardcoded C++ rules to neural network-based learning)

- Exception handling – Handles edge cases without requiring explicit programming for every scenario

- Cross-system orchestration – Coordinates workflows across different clouds, applications, and legacy systems

Real example: An invoice dispute arrives via email. Traditional RPA could extract data from a standardized form but couldn’t read the unstructured dispute explanation, compare it against varied contract language, determine the appropriate resolution, and draft a contextual response. AI agents can handle all of this – and UiPath’s platform orchestrates the entire workflow, using different AI models (Anthropic for reading, OpenAI for reasoning, Microsoft Copilot for finding files), traditional bots for data entry, and routing to humans when needed.

Microsoft Copilot alone can’t execute this end-to-end because it works primarily within the Microsoft ecosystem. UiPath’s value is coordinating everything across multiple systems and AI providers.

The Agentic AI Product Suite

UiPath launched four interconnected AI automation products in 2025:

- Autopilot – Conversational AI interface for business process automation

- Agent Builder – No-code/low-code platform for creating custom AI agents

- Maestro – Orchestration engine that coordinates AI agents, RPA bots, and human workflows

- Agentic Testing – AI-powered quality assurance and testing capabilities

Current Adoption Metrics

As of Q3 FY2026, the adoption indicators are encouraging:

- 950+ companies developing AI agents on the UiPath platform (more than doubled from the previous quarter)

- 365,000+ processes orchestrated using Maestro

- ~3,000 agents created during the private preview phase

Use cases span invoice processing, customer service, fraud detection, claims processing, and healthcare operations.

Revenue Timeline and Management Guidance

It’s important to understand the gap between pilot adoption and revenue recognition, as well as UiPath’s fiscal year calendar.

UiPath’s Fiscal Year Structure:

- Fiscal Year 2026 (FY2026): February 1, 2025 to January 31, 2026

- Fiscal Year 2027 (FY2027): February 1, 2026 to January 31, 2027

As of this writing (February 2026), FY2026 has just ended and FY2027 has just begun.

Most current users are in trial or pilot phases. Enterprise software typically follows this adoption curve:

- Trial/Pilot Phase: Companies test functionality with limited scope (minimal or no revenue)

- Budget Approval: Internal business case development and procurement process

- Production Deployment: Initial enterprise contracts

- Scale and Expansion: Broader rollout across organization

This cycle typically spans 12-18 months from initial trial to material revenue contribution.

Management has been explicit about expectations:

March 2025 (Q4 FY2025): “We don’t expect [AI] to be a material contributor to revenue in fiscal year 2026.”

June 2025 (Q1 FY2026): “FY2026 is viewed as a foundational year for meaningful new revenue streams in FY2027 and beyond.”

December 2025 (Q3 FY2026): “Adoption is early and not expected to materially contribute to fiscal 2026 topline yet.”

The implication: FY2027 (which began February 1, 2026) represents the expected inflection point where AI automation should begin contributing materially to revenue growth.

Critical timing note: We are currently at the start of FY2027. This means the fiscal year where management expects AI to materially contribute to revenue is happening right now. The first evidence should appear in Q1 FY2027 earnings (to be reported around June 2026, covering the February-April 2026 period).

Investment Thesis and Considerations

My investment thesis centers on UiPath successfully transitioning from a mature RPA platform to a broader AI orchestration layer, with FY2027 representing the critical proof point.

Based on management guidance and the pilot-to-production timeline, I expect significant revenue contribution from AI automation beginning in FY2027 (fiscal year starting February 2026).

If AI revenue remains insignificant through FY2027 and beyond, this would contradict the core investment thesis and warrant reconsidering the position.

Key Success Factors

Several factors will determine whether the thesis plays out:

Pilot-to-Production Conversion: The 950+ companies currently developing agents need to convert to paying enterprise customers at reasonable rates (30-50% would be healthy).

Average Selling Price Expansion: AI-enabled contracts should command higher pricing than traditional RPA (ideally 2-3X) as they address more valuable use cases and expand the automation scope.

Net Revenue Retention Re-acceleration: NRR should stabilize and begin increasing as AI capabilities drive customer expansion beyond the traditional RPA ceiling.

Competitive Positioning: UiPath needs to demonstrate wins against Microsoft Power Automate and other competitors in cross-platform orchestration scenarios.

Key Risks to Monitor

Execution Risk: Slower-than-expected conversion from pilots to production deployments would delay or prevent the FY2027 revenue inflection.

Pricing Pressure: If AI automation becomes commoditized quickly, ASPs may not expand as anticipated.

Competitive Dynamics: Microsoft or other competitors may develop “good enough” solutions that satisfy most enterprise needs at lower price points.

Technology Risk: New AI-native platforms may offer superior orchestration capabilities, or open-source alternatives may emerge.

Market Risk: Enterprises may standardize on single-vendor AI solutions rather than requiring multi-model orchestration, reducing UiPath’s value proposition.

Valuation: My Financial Model and Projections

Let me walk you through how I’m thinking about UiPath’s potential returns over the next 6 years.

Starting Point: Q4 FY2026 (Reporting Soon)

Management guided:

- Revenue: $462-467M

- Non-GAAP Operating Income: ~$140M

My assumptions for Q4:

- Revenue: $465M (midpoint)

- GAAP Operating Income: $65M

- Gross Margin: 85%

When we add up the full FY2026, this gets us to about $50M in GAAP operating profit for the year – the first time UiPath achieves full-year profitability.

Recent Growth Trajectory

In my opinion, UiPath’s revenue growth has been decelerating as traditional RPA matured:

- FY2023: +13.9%

- FY2024: +10.5%

- FY2025: +10.1%

- FY2026: +11.5% (forecast)

The question: Does AI reverse this trend?

Three Scenarios for FY2027-2031

I’ve built projections under three different outcomes:

| Scenario | Annual Growth | FY2031 Revenue | FY2031 Op Income | Op Margin | What This Means |

| Bear | 10% | 2.6b | 5,83m | 23% | Agentic AI doesn’t materialize, slow growth continues |

| Base | 20% | 4.0b | 1,774m | 45% | AI monetizes successfully, NRR re-accelerates |

| Bull | 25% | 4.9b | 2,537m | 52% | UiPath dominates AI orchestration market |

Key Assumptions (All Scenarios):

- Gross margin: 85% (maintained)

- Operating expenses: $1.6B by FY2031 (up from current $1.3B)

How Revenue Builds Year-by-Year

| Year | Bear | Base | Bull |

| FY2026 | $1.6B | $1.6B | $1.6B |

| FY2027 | $1.8B | $1.9B | $2.0B |

| FY2028 | $1.9B | $2.3B | $2.5B |

| FY2029 | $2.1B | $2.8B | $3.1B |

| FY2030 | $2.3B | $3.3B | $3.9B |

| FY2031 | $2.6B | $4.0B | $4.9B |

Target Prices: Combining Growth × Multiple

Current stock price: $13 Current valuation: ~10x operating income

Here’s what the stock could be worth in FY2031 under different scenarios:

| Multiple | Bear | Base | Bull |

| 15x | $15.38 | $46.75 | $66.89 |

| 20x | $20.51 | $62.34 | $89.19 |

| 25x | $25.63 | $77.92 | $111.49 |

| 30x | $30.76 | $93.51 | $133.78 |

What This Means in Returns

From today’s $13 price:

| Scenario | My Expected Outcome | Target Price | 6 Year Return | Annualized |

| Bear | Agentic AI Fails | $15.38 (15x operating multiple) | +18% | 2.8% CAGR |

| Base | Agentic AI Work as planned | $62.34 (20x opeerating multiple) | +380% | 29.9% CAGR |

| Bull | Agentic AI dominates | $111.49 (25x operating multiple) | +758% | 43.1% CAGR |

My Risk/Reward Assessment

At $13, the setup looks attractive:

- Downside: If AI completely fails → still get 2.8% CAGR (company remains profitable)

- Base case: If AI monetizes reasonably → 30% CAGR

- Upside: If execution is exceptional → 43% CAGR

The asymmetry favors being positioned for the base case while the bear case provides some floor.

My Conviction Level: Cautiously Optimistic

I want to be transparent about my conviction in this investment. Unlike some of my highest-conviction positions, UiPath scores mixed on my investment framework:

1. Does the CEO Have a Bold, Ambitious Vision? -So so

Daniel Dines has built a successful company, but the vision feels somewhat constrained. UiPath is focused on enterprise automation – a valuable but defined market.

Compare this to:

- Elon Musk (Tesla/SpaceX): Sustainable energy + multi-planetary species

- Jeff Bezos (Amazon): Everything store + cloud infrastructure + space

- Sundar Pichai (Google): Organizing world’s information + AI everywhere

UiPath’s vision doesn’t extend into adjacent massive markets or aim to fundamentally reshape how we work and live. It’s a “best-in-class automation platform” rather than a “change the world” vision.

This matters because the most extraordinary returns often come from founders with seemingly impossible ambitions who refuse to be constrained by current market definitions.

Impact on thesis: Limits upside – even if perfectly executed, UiPath likely remains a great automation company rather than becoming a generational, culture-defining platform.

To be fair, Daniel Dines has executed well within the RPA domain and demonstrated solid leadership. However, his success has been aided by favorable market conditions:

- Limited competition: The RPA market hasn’t attracted many world-class competitors. Most automation players either stayed niche or were acquired.

- Microsoft’s strategic choice: Microsoft has chosen to keep Power Automate within their ecosystem rather than aggressively competing for cross-platform automation. They seem content dominating Microsoft-to-Microsoft workflows, leaving the heterogeneous enterprise market to UiPath.

This competitive landscape gave UiPath room to establish dominance somewhat by default.

The market size ceiling concern:

Even if UiPath captures the entire automation market – both structured and unstructured data processing – there’s a fundamental constraint: companies only pay so much to save costs.

Automation is primarily a cost-reduction play. Unlike revenue-generating platforms, there’s a natural ceiling to how much enterprises will invest. Once you’ve automated 70-80% of automatable processes, incremental spending drops dramatically.

The “what’s next?” problem:

This is my biggest concern about UiPath’s long-term trajectory. After they dominate enterprise automation, then what?

Compare UiPath’s roadmap to Tesla’s:

- Tesla: Model S → Model 3/Y (scaling cars) → Full Self-Driving (software/AI) → Optimus (humanoid robots) → Energy storage

- Each success opens adjacent multi-trillion dollar markets

- Clear 20+ year growth runway across different domains

- UiPath: Traditional RPA → AI-powered automation → … ?

- Growth curve is entirely within automation

- No obvious adjacent markets being pursued

- After capturing automation, the path becomes murky

The innovator’s dilemma risk:

When you’re the market leader focused on winning your current category, you risk missing the next wave. History is full of examples:

- Blockbuster optimizing video rental while Netflix redefined entertainment delivery

- BlackBerry perfecting physical keyboards while Apple redefined what a phone should be

- Nokia dominating mobile phones while smartphones emerged

My concern: While UiPath perfects automation, a smaller, more aggressive company might capture adjacent markets that automation enables. Or the entire category gets disrupted by something we haven’t imagined yet.

Investment implication:

This could be a great 5-year investment (capturing the automation market), but I’m uncertain about the 10-15 year outlook. Without expansion into adjacent markets or a more ambitious vision, UiPath hits a growth ceiling even if they execute perfectly.

This is why it’s not my highest-conviction holding – it’s a good company in a good market, but potentially not a generational compounder.

2. Does the Company Have World-Class Execution?- So so

UiPath has defended its market position well, maintaining leadership in RPA against numerous competitors. Management has successfully transitioned the business model from license to subscription and achieved profitability.

However:

- The competitive moat isn’t unassailable. Microsoft, ServiceNow, and others have credible automation offerings

- The AI transition is unproven. We won’t know if management can execute the pivot to AI orchestration until FY2027 results materialize

- Growth has decelerated significantly from 40%+ to low teens, suggesting execution challenges in finding new growth vectors

UiPath has good execution, but not exceptional execution.

Impact on thesis: Increases risk – the AI transition requires excellent execution to succeed, and historical performance is mixed.

3. Does It Have a Clear and Probable Path to 10X?- Probable, But Not Crystal Clear

The math works:

- Current price: $13

- 10X target in 10 years: $130

- My bull case (25% growth, 25x multiple): $111 in 5 years!

But it requires everything to go right.

What gives me comfort: Even in the bear case where AI completely fails, I estimate minimal losses. The current $13 price with $50M in GAAP operating profit and $1.4B cash provides a floor. Worst case might be 2-3% annual returns rather than catastrophic losses.

4. Does It Have a Superior Product and the Ability to Defend That Superiority? -Yes for Now, Uncertain for the Future

Current state: UiPath has the best RPA platform with the strongest enterprise features, most integrations (6,000+ apps), and deepest institutional knowledge. The product is genuinely superior to alternatives today.

The uncertainty: Product superiority is backward-looking. Valuation is forward-looking.

We’ll have answers in the next 2 quarters.

Summary: Why I’m Invested Despite Mixed Conviction

This isn’t my highest-conviction investment, but it’s in my portfolio because:

- Risk/reward is asymmetric – Limited downside, significant upside if AI works

- Timing is favorable – We’re at the inflection point where AI should materialize

- Optionality is valuable – If UiPath cracks AI orchestration, returns could be exceptional

- Downside is protected – Profitable, cash-generative business provides a floor

I’m sizing this position appropriately for a “probable but uncertain” outcome rather than a “high conviction” bet.

What would increase my conviction:

- Evidence of AI revenue scaling (Q1-Q2 FY2027)

- Clear competitive wins against Microsoft

- NRR re-acceleration above 110%

- CEO articulating a bolder, more expansive vision

What would cause me to exit:

- AI revenue remains negligible through FY2027

- NRR drops below 100% (indicating customer contraction)

- Gross Profit Margin goes below 80%

I’ll reassess conviction every quarter as new data emerges.

Conclusion

UiPath faces a critical transition period. The traditional RPA business has matured, reaching natural saturation points in existing customer deployments. The company’s future growth depends on successfully expanding into AI-powered automation that can address unstructured data and judgment-based workflows.

The fundamental question is whether enterprise automation orchestration becomes a commoditized capability (favoring bundled solutions) or remains complex enough to justify specialized platforms.

I believe heterogeneous enterprise environments – spanning multiple clouds, diverse applications, various AI models, and legacy systems – create genuine demand for sophisticated, platform-agnostic orchestration.

However, this remains a show-me story. FY2027 (beginning February 2026) represents the critical inflection point where the AI transition should materialize in financial results. The next 12-18 months will reveal whether UiPath can successfully monetize its AI strategy and return to meaningful growth.

I’m positioned accordingly, with clear metrics to evaluate progress and a willingness to adjust the thesis as new information emerges.

Disclosure: I own shares of UiPath. This represents my personal analysis and is not investment advice. Please conduct your own research and consult with financial professionals before making investment decisions.