{kind=link}

Lately, I have seen many bloggers and local YouTubers dive into the world of options, so I have decided to join in the fray. The world of options has been my playground for the past few months as I have been learning and doing some paper trading on the Thinkorswim platform. However, nothing could beat putting my chips on the table: the simulated trading experience was incomparable to investing with my own cold hard cash. Because no money was involved in paper trades, I lacked the financial discipline to monitor it on a daily or regular basis; hence, it wasn’t easy to pick up the ropes of option trading.

For me, the biggest hurdle in starting to trade was finding out how to transfer funds into Thinkorswim. I believe it’s the same for new investors who have yet to start trading because picking the right brokerage account and puzzling out the paperwork is sort of a road block. After I intentionally set aside time to figure out how to wire funds and shares to TD Ameritrade, I started my first call option, and the rest was history.

Today, I will share a recent covered call strategy on Nio, which potentially gives a good return on investment. It takes two steps to execute a covered call strategy, by first buying shares of Nio, and selling out of the money call option at a higher strike price.

This is a ‘gamble’ with $3,333* on the line: whether or not I succeed in this bid depends on one of two outcomes.

If option expires out-of-the-money (OTM) or at-the-money (ATM) → I win (Nio shares go below $40 USD )

If the option expires deep-in-the-money → I lose. (Nio shares go above $40 USD)

*3.33k was derived by (Nio’s share price – premium of the Call option) .

In my case, I added Nio shares at $36.09 USD and wrote a long-dated call option expiring on Jan 2022 at a strike price of $40 USD for a premium. By selling a call option, the buyer has the right to purchase Nio shares from me at the strike price of $40 USD before expiry. As an option seller, I hope that Nio shares will not shoot past $40 USD so that the option expires worthless and I can keep the premium and repeat the whole process.

I will elaborate on a few scenarios that my option could play out in the subsequent paragraphs.

Why Nio?

Being a loss-making company, Nio probably won’t fit the bill as a great company to own; even growth investors would arguably prefer Tesla. However, when it comes to options investing, great fundamentals are only part of the equation, and there are many other factors to look out for.

High Implied Volatility

There’s an adage among traders: the trend is your friend, until the end when it bends. If you are an option seller, implied volatility (IV) is probably your friend. In short, you get paid a better premium upfront for writing options when the IV is high.

For Nio, its implied volatility has always been stubbornly high at a 60% range, and at an IV of 64.03 %, its IV percentile is only at 6% , which means it is trading below 64.03% IV only 6% of the time.

IV Percentile is a term used to measure its current implied volatility compared to the IV value in the past. Here’s the formula to determine one year IV percentile

No of trading days below current IV/ Total trading days (250)

For instance, if Nio’s Implied volatility is hovering at 60%, and in 200 out of the 250 days, Nio’s IV has been below 60%, Nio’s IV percentile translates to

200/250= 80%.

Low Cash Outlay

Although Tesla options also trade at high IV, I am not prepared to buy and hold 100 Tesla shares at current prices, which brings us to the next reason why Nio was a better choice for a covered call strategy. To give you some context, one option contract represents 100 shares of an underlying security, and owning 100 Tesla shares cost $79k USD. Comparatively, each share of Nio costs me $36 and only requires a cash outlay of $3,609 USD to own 100 Nio shares.

High Return on Investment (ROI)

Instead of selling a monthly date to expiration (DTE) put option, I wrote an out-of-the-money (OTM) put option, at $40 USD strike price, expiring in Jan 2022. First, I bought Nio shares at USD 36.09, and at the same time, sold a call option for $276 USD.

ROI= 2.76/36.09 = 7.65% in 105 days.

Annualized return= [1.0765^(365/105)-1 ] * 100% = 1.292-1= 29.2%

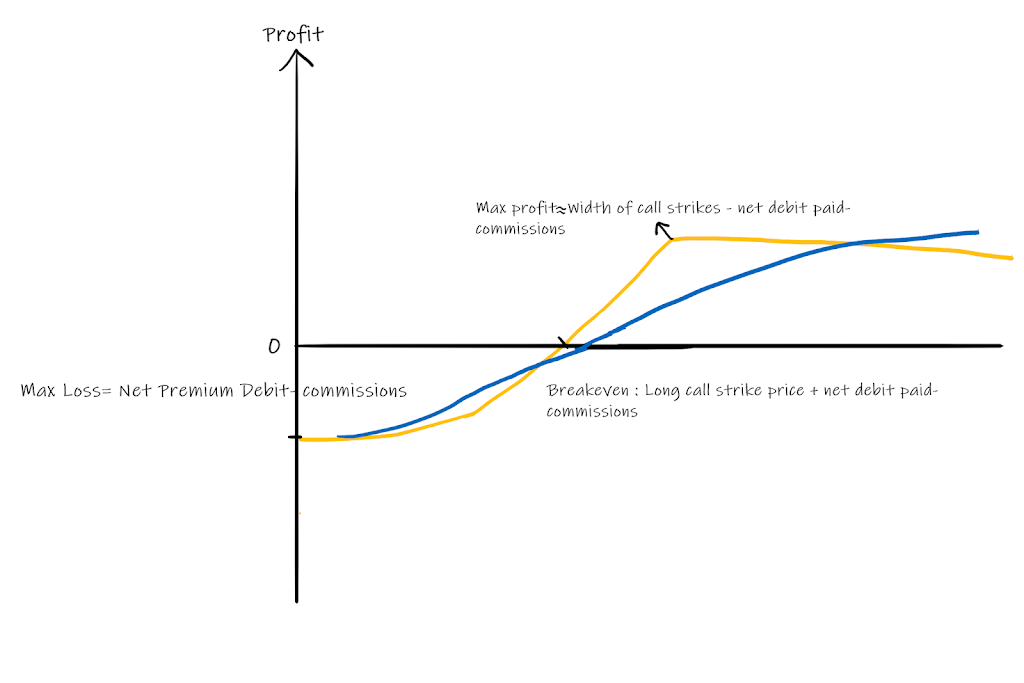

This is how my profit and loss chart looked like.

Possible Scenarios

- If the option expires deep-in-the-money → I lose. (Nio shares go above $40 USD)

If the above scenario plays out, I am obligated to sell my Nio shares to the option buyer at $40 USD and keep the option premium.

In the most optimistic scenario, I could achieve a max gain of $667 USD, which is derived from Option Premium+ (Strike price minus the price I bought the share at) = 276+ 4000-3609. If this scenario were to happen, I would walk away with $667 USD.

On the other hand, if I wish to buy back Nio shares, I can purchase it directly on the stock exchange or write a cash secured put. Selling the put option obligates me to buy the share at the specific strike price if assigned; however, if it expires OTM, I get to keep the option premium and repeat the cycle, essentially getting paid while I wait.

Another strategy is to roll my options. Before the option expires ITM, I will close my current call option (at a loss or a very small profit) and sell another OTM call at a higher strike price with a longer DTE. Ideally, the new option premium will be able to cover the losses incurred from the previous call option. I will utilize this strategy if I wish to hold on to Nio Shares.

2. If option expires out-of-the-money (OTM) or at-the-money (ATM) → I win (Nio shares go below $40 USD )

If Nio trades below $40 USD on 21st Jan 2022, the call option will not be exercised, and $276 USD is mine to keep. This effectively brings down my breakeven price/share to price I bought the share minus option premium ($36.09-0.276) = $33.33 and I am free to write another OTM call option to further drive down my average buy price.

If shares of Nio continue its downtrend, it portends that its shares will trade at or likely below $40 USD and I get to keep the premium. That’s the main objective of an option seller since this strategy forfeits the upside potential of the stock in exchange for an income. By writing a covered call, the investor believes that the stock price is unlikely to go above the strike price in the short term. If Nio prices hover at current levels, I would do another covered call strategy and collect premiums.

Option Risk Graph

Notice that there are two distinct line graphs. The yellow line represents the amount of profit/loss at different share price points on the expiry date. The maximum loss I will incur is $3,333 USD if Nio shares go to 0, and I get to keep the option premium.

Whereas the profit/loss on day 0 is depicted by the blue curved line. The blue line will converge to the yellow line as it approaches the expiration date because the option loses its extrinsic value due to time decay. Its daily implied volatility could also affect the profit and loss curve, but I will leave that for another day. In short, as an option seller, time decay works in my favour.

Here are two more suggested ways to trade option with a lower cash outlay.

Method 1: Bull Put spread

Instead of buying the shares, you are buying a put option to minimize the downside risk if shares drop.

Like covered calls, Bull Put spread involves a two-step strategy.

1. Sell an OTM put option and collects a premium

2. Buy another OTM put option at a lower strike price with the same expiration date and pays a premium

Executing this credit spread should yield a net premium as the profits from selling put options should easily offset the costs of buying the put option. If both options expiry OTM, consider replicating this cycle to collect passive income.

While the method reduces the cash outlay compared to covered calls, investors will have to suffer a real loss if the share price sank below the lower option strike price upon expiry.

Another drawback is that the net premium collected is lesser as compared to covered call since there is a price to pay for buying put option.

Method 2: Diagonal Spread a.k.a. Poor man’s covered call.

1. buying a deep ITM call option with 6 months or more DTE

2. selling monthly OTM put option

Instead of paying for the hefty price of owning 100 shares, he buys a deep in the money call option with six month’s expiry or more which serves as a collateral. The call option should have a high delta i.e., above 0.7 since it is deep ITM.

Next, you can start selling an OTM put option with one-month DTE and repeat the cycle when put options expire worthless.

Don’t expect high returns for such a strategy, and 1% return a month would be ideal. The last 30 days of a put/call option has the highest rate of time decay, hence one who uses such strategy would be able to earn a premium on the time decay.

However, I wouldn’t recommend this strategy on stock with high volatility as the premium for the deep ITM call option will be quite expensive due to high IV. A few stock suggestions for using a poor man’s covered call would be TLT, Microsoft and Apple.

Thank you so much for spending time to read my blog and I really appreciate you. If you enjoyed reading my blog, hope you can support me by liking my Facebook page here or share my post. You may also follow my Twitter account here, where I post my buy and sell transactions. Currently, I do not earn any fees through any affiliate programme or sponsor. If you have any queries, feel free to post them and I am happy to take questions! 🙂