It’s been 6 months since I last updated my portfolio.

I realize time flies so quick once working life started. I told my church friends about it and they said it will get even faster after I turn 30. On top of just updating my portfolio,

I also wrote about Stock Monthly Investment Plan (SMIP) for those who

wish to do dollar costs averaging in HK and also my goals

before hitting 31.

Sharebuilders Plan. (commitment of $2,000/ mth)

month since Sept last year after getting more disposable income. I also found

that valuation for ST Eng and STI pretty attractive.

PE ratio for Straits Times Index (STI) is 11.6. Compared to Hang Seng Index at

16 and Dow Jones Industrial Average at 26.57, STI still has long way to go. I

have thoughts of reducing the monthly commitment to $1,000 a month as I applied

for Kim Eng Monthly Investment Plan and SMIP with HSBC HK but will consider

scaling down when STI goes above pe ratio of 15. For ST Engineering I am still

sitting at a loss but I believe will do just fine for long term investment.

reinvestment. As I am in my stage of building my wealth, I would rather

maximize my return my reinvesting my dividends for a small fee.

I was a university student and working part time. It was the time when my parents officially handover all my Angpow proceeds to me and it has been sitting on

very little interest in that bank account. Since then the plan has been on GIRO. I last

checked in Oct 17 and the bank account has started to dry and I decided to

continue funding that account via my salary account. I could have merged it with Share Builder to

save costs and so but decided to keep it that way for sentimental reasons.

$500 monthly)

stock price has been going upwards after a small dip at 300 HK$ levels. It’s

hard to do valuation and calculating it probably won’t make much sense too,

especially pe ratio is at its 57. To me, its safety margin is its ability to accelerate growth and I continue to believe in its growth story.

6000 HK$ monthly i.e. $1,000 monthly)

trip to HK for Christmas. Back then, I was searching for an investment plan

which allows me to DCA for Hong Kong Index. Turns out that HSBC and a many HK

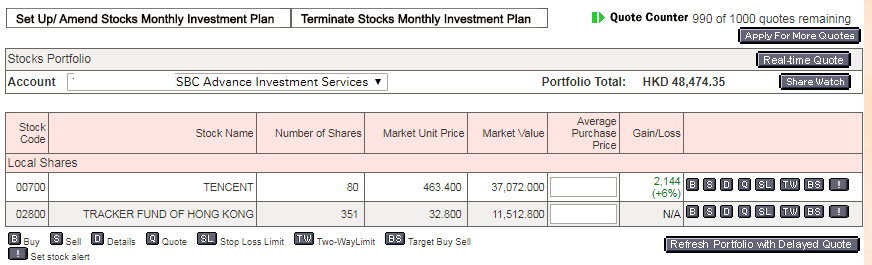

banks allow me to do so. The stock code for it is 2800, Tracker Fund of Hong

Kong. You can check out the Fund Factsheet here .It

tracks the index pretty well with only tracking error of 0.0514%. I invested a lump sum of 5,000 HK$ and monthly investment of 6000 HK$, i.e. 1,000 SGD/month . As a non-HK resident, the only downside is the inconvenience

to convert and transfer money to HK$. For those who are keen to invest through HK

banks, also do note that most Singapore banks charge a transfer fee and

foreign transaction fee hence the best way for me is to change HK$ in

local money changers and deposit into HK bank account. My relatives and I travel to HK often so won’t be much of an issue.

investment plan, or 月供股票 they

call it. Currently, HSBC is undergoing a promotion where handling fee and

brokerage fees etc, are waived and only charge a monthly Custodian Fee of

25 HK$ (note that dividend handling fees/ corporate action fees do apply). I

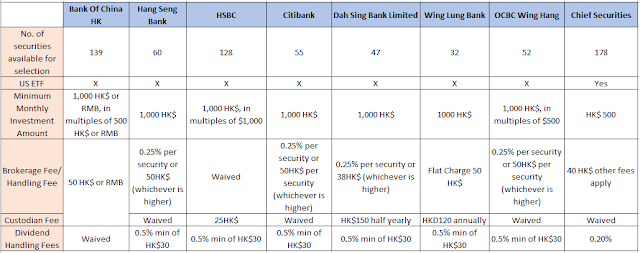

did up a comparison table on the plans offered by banks and brokerage

firm. On top of banks, I included Chief

Securities because they are the only firm which offers DCA for US ETF- Vanguard

S&P 500 ETF (3140). Another way to DCA US ETF is to open a Standard Chartered

Priority Banking account with brokerage fee of 0.2%, no min brokerage fee.

|

| Comparison chart for banks/brokerage firms offering stock monthly investment plan. |

{kind=link}

Do note that the promotions , fees, and securities available for investment may change with time. If you are viewing this few years after this post was published, kindly refer to their respective website for more updated info.

shares 0700:HK in 2 batches: 40 at 436.60 HK$ and 40 and 457.40 HK$. This is in

addition to the Maybank Kim Eng Monthly Investment Plan. For those new

to Tencent Holdings, its owns a popular messaging app, WeChat and it started listing at 3.7 HK$ in 2004 and current price of

460 HK$ has been adjusted for 1 to 5 shares split on 2015. It’s PE ratio of 57

seems very rich, but richly priced stocks can actually defy gravity and

continue to rise for a prolonged period of time. When a stock is hot and

everyone is clamouring to buy, the stock can continue to sustain lofty

valuation. After all valuation is a guide, and if there is any safety margin to

talk about, it would be its strong growth.

STI returning 22.08%. My portfolio main drivers are OCBC and DBS shares bought during at

2014 and 2015 and I still remained committed to holding them. Back

in 2016, I sold most of my shares for property investment which didn’t

materialize and managed to buy back subsequently to ride on the bull run. Due

to much work and travel, I have not been actively managing my portfolio but I

am quite blessed with banks and property stocks boosting my overall portfolio

returns.

and my investing approach is more of a buy and hold. I do my best to pick

stocks with good fundamentals and invest for the long haul i.e. companies which

have economic moats that I can hold for many years. In times when the stocks or

general market seemed overvalued, I may continue to hold them. Over the years,

I realized that I have made more money holding on to the winners that cashing

out on my early profits.

find, and if I were to sell away a stock and my expectations about future lower

valuation does not actually materialize, I might have missed one big boat. One

example would be Riverstone. I bought them at $0.485 and sold at $0.585, and

the feeling was great until it went to $1.10 after 1 for 1 bonus issues and many

rounds of dividends. Similarly, I am certain that there are times Coca

Cola shares are overvalued but if one continues to hold a share of Coca Cola

trading at $40 in 1919 is now worth $9.8mil.

it out here.

anticipation of a lower valuation to come, it equates to leaving a business

that I know well; or business with developments which I can interpret with some

levels of confidence. If the price continue its upward trajectory after selling

and I am unable to re-enter, I may have to find new companies and opportunities,

and that means spending additional time to do research and bring the

understanding of the companies to a similar level.

and out companies with poor fundamentals selling at dirt cheap price expecting

a turnaround situation. The time that I will sell my stocks is when the

company’s fundamentals starts to deteriorate, especially when free cashflow

becomes negative or a dividend cut.

stock which I got it during IPO. The prospectus showed growing revenue trends,

increased FCF, experienced management and overwhelming support from

institutions. However, the results reported lower revenue, decrease in net

profit and even negative FCF. The only saving grace is lesser debt. Though the

lack of price movement after earnings release suggested that the price must

have factored into the earnings prior to the report, I felt that I don’t really

understand the company well enough. So, I divested to lock in some small

profits.

anyone who trades or does short term investment. It’s just that buy and hold

suits me better especially when I have very limited time to monitor my portfolio.

Everyone should find their own investment strategy which suits them best.

June 2017

|

| Buy/sell Transactions |

|

| Dividends Collected (page 1) |

|

| Dividends Collected (page 2) |

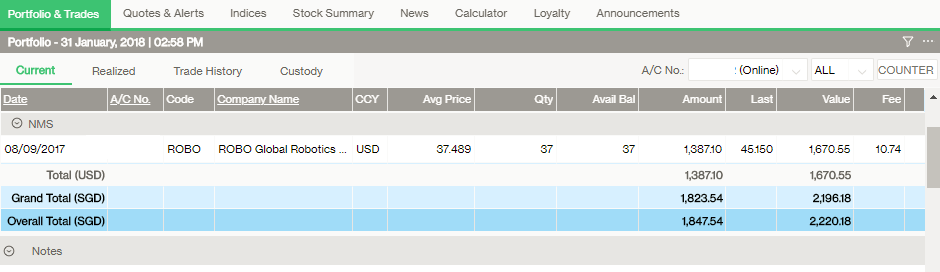

Automation ETF at US$37.20.

ComfortDelgro. Its recent tie up with Uber has drawn much mixed reactions but

whether it will yield positive results is anyone’s guess. For now, I will continue

to hold for its dividends and I am pretty sure they can sustain its dividend

with payout ratio of about 0.7. At the price of $2.08, its yield is close to 5%.

weakness for the long term. The reason for its underperformance was due to its

stagnant growth coupled with softening medical tourism. Its catalyst for

growth is in the opening of Chongqing and Shanghai Hospitals. In my view, till

they began operation, profit will continue to stay muted. Even when they began

operations, it will also take few years for its business to breakeven. Hence,

it is not a stock for short term. Its price of $1.12 translates to a pe ratio

of 28 which is attractively priced in my view considering that it is a

defensive sector and serves as a good hedge for rising healthcare costs.

POSB Invest Saver =$10,292

MayBank Kim Eng Monthly Investment Plan=$468

HSBC SMIP =$10,365

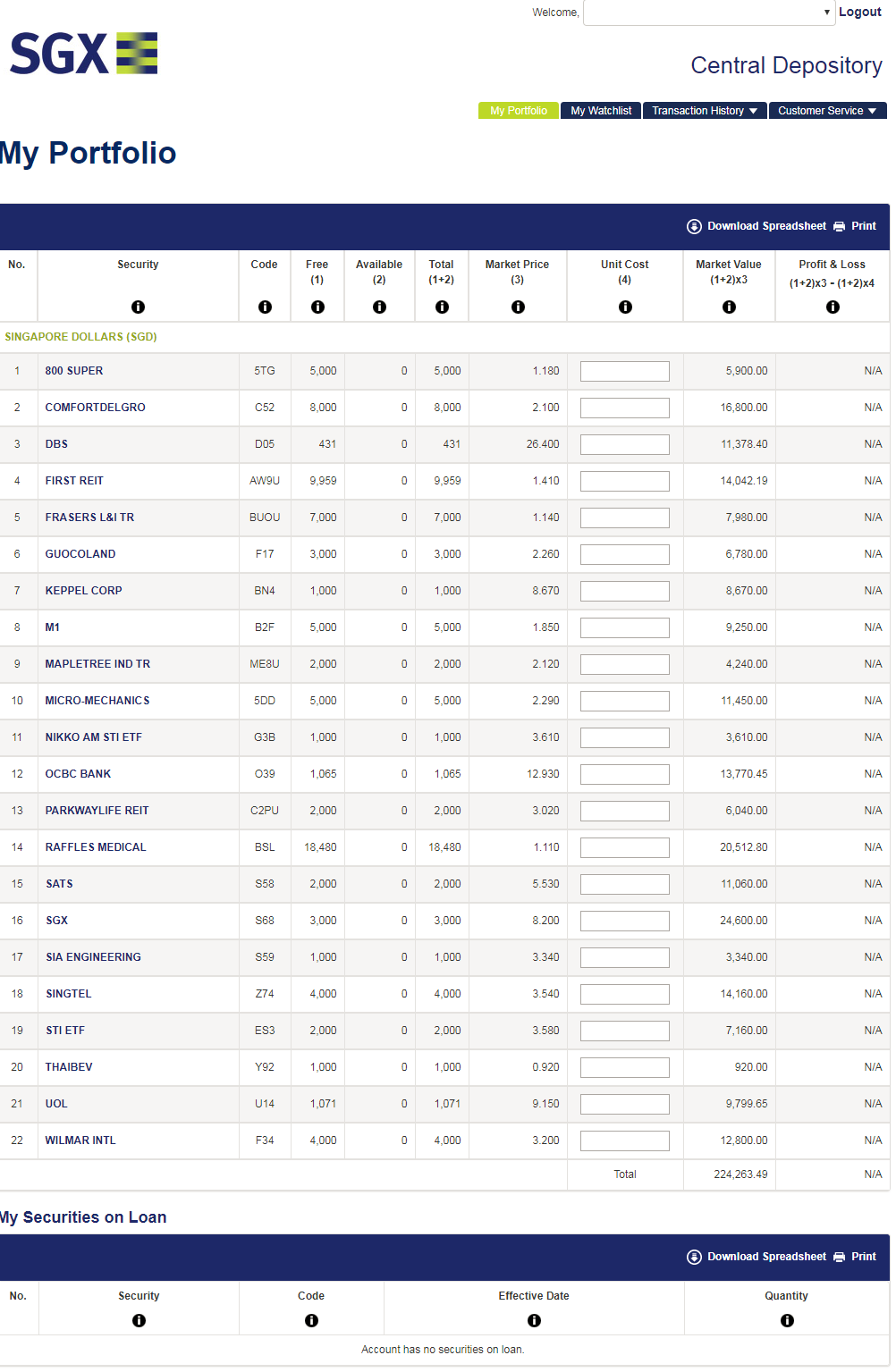

SGX Portfolio 1= $224,263

SGX Portfolio 2= $119,195

Standard Chartered Online Trading Acc=$2,220

Cash= $30,000

wind is favourable. At best, the crew can navigate to stop crashing into

things, but the ship could just be mindlessly floating in the middle of the

ocean.

a goal in mind, or any targets to achieve, we will behave like a ship which

floats through life but goes nowhere in particular.

setting. The first one is about setting S.M.A.R.T. goals: Specific, Measurable,

Achievable, Relevant and Timely. Then the goals can be broken down into small

steps which can be achievable daily so we can track our progress. Another

school of thought believes in setting goals which can be unachievable or unrealistic through visualizing your success daily that you have achieved your goal. This will trigger your creative subconscious

mind which will generate ideas and means to achieve your goal. It makes you more

motivated, energized and looking forward to every new day. This is not unproven

or merely daydreaming as Michael Jordan had always visualized himself taking the

last shot before he ever took one in real life and Muhammad Ali had also imagined himself victorious in life even before the fight began.

also use a combination of both methods.

financial goals. Currently, my stocks portfolio is about $400k and my goal

is to reach $1 million before hitting 31. Assuming dividend yield of 5%, that would generate about $4.2k/mth of passive income, which will

cover about 80% of my monthly expenses (see below). It’s also an easy number to

remember and a good 7 digit target to look forward to.

months to go. I can work hard to earn a more income, do more research for

better stock picking skills, or be more disciplined with money but the rest

would be up to how the stock market performs. I can’t eliminate systematic

risks or predict the next financial crisis.

depend on how STI performs or the indices of the countries I am investing in.

Food/Transportation/Tithe/Parental allowance = $2,200 mth

Income Tax/ Medisave contribution= $1,100 mth

Insurance premiums (Protection and savings & investment plans)= $1,500/mth

Travel= $3,600/ year i.e. $300/mth

Buy more each transaction

When my stocks perform well, my total

profits aren’t substantial because I only bought 2000 or 3000 shares. Since I

spent much time to do research on a particular stock, I should be more confident about it. I bought 5,000 shares of MicroMechanics at $1.035 in April with 120% till date. However it only consisted only 2.75% of my overall portfolio and my hard work resulted in insignificant gains. I had a writeup on Micromechanics which you can check it out here.

On top of the returns, buying more also reduces my transaction costs as a

percentage of total value.

Investing more Aboard

To improve my returns further, I will be increasing my position in US and

Hong Kong shares to have more exposure to growth stocks, especially ETFs tech

companies. Last year, Hang Seng Index achieved gains of 35.99%

compared to STI returns of 22.08%. Its stellar performance was partially due to

gains from Tencent, which constitutes 11.57% of index(before 1st Dec

2017), returning 124.91% over a year. Subsequently, it had a quarter rebalancing and the stock weighing on Hang Seng

Index dipped to 10%.

It’s almost 10 years since our last financial crisis and US market has been on

a bull run since then, with Dow Jones Industrial Average (DJIA) exceeding its

previous high of 15,000 points by 70%. In comparison, local markets are still

having a hard time matching the performance. Hence, having exposure to foreign

markets helps to boost my portfolio when local markets are facing downward

pressure or any possible geopolitical risks.

There are definitely risks to investing overseas, such as currency volatility,

or even taxes on dividend gains, but my view is that the benefits in general

outweigh the risks.

$1mil, you may follow/Like my Facebook page here. I will update my Facebook on

any new posts.

Technique:

https://www.nikkoam.com.sg/files/documents/funds/fact_sheet/sti_etf_fs.pdf

Enjoyed your posts so far. Plenty of food for thought. Look forward to your next post

Thanks INTJ!