Hi all, this is really a long post (warning), here are the subtopics I will be discussing.

- History of MNAC Trust

- Determine the Discount Rate via Capital Asset Pricing Model

(CAPM) - Determining Net Profit Margin (NPI)

- Derive the ratio of NPI to Distributable Income to Shareholders

- Analysis of Japan Properties Acquired in 2018

- Analysis of MBP and OPB (Japan Properties Acquired in Dec

2019) - Analysis on Sandhill Plaza

- Analysis on Gateway Plaza

- Analysis of Festival Walk

- Summing up altogether+ Intrinsic Value

1. History of MNAC Trust

Festival Walk

Festival walk was developed jointly in 1998 by Swire and

Citic Pacific and back then it was once the biggest shopping mall in HK once

opened. It was then owned by Swire Properties and bought over by MNAC’s current

sponsor Mapletree Investments @ 18.8 Billion so Swire Pacific could focus on

investments in Mainland China in 2011.

Citic Pacific and back then it was once the biggest shopping mall in HK once

opened. It was then owned by Swire Properties and bought over by MNAC’s current

sponsor Mapletree Investments @ 18.8 Billion so Swire Pacific could focus on

investments in Mainland China in 2011.

Gateway Plaza

It was used to be known as Beijing Gateway Plaza and it’s

situated at one of Beijing’s core business district. The building was completed

in 2005 by Bestride and sold to HK Gateway in 2006. About a year later, Tin

Lik, sold shares of Beijing Gateway Plaza (BVI) Limited which holds HK Gateway

to RREEF China Commercial Trust. In April, Gateway Plaza was then acquired by

Mapletree India China Fund at RMB 2.1bil, a private real estate fund belonging

to Mapletree Investments Pte Ltd (MIPL).

situated at one of Beijing’s core business district. The building was completed

in 2005 by Bestride and sold to HK Gateway in 2006. About a year later, Tin

Lik, sold shares of Beijing Gateway Plaza (BVI) Limited which holds HK Gateway

to RREEF China Commercial Trust. In April, Gateway Plaza was then acquired by

Mapletree India China Fund at RMB 2.1bil, a private real estate fund belonging

to Mapletree Investments Pte Ltd (MIPL).

In 2013, the Sponsor launched Mapletree Greater China Commercial

Reit in 2013, consisting of the above two properties. In 2015, the Reit

acquired Sandhill Plaza at RMB 1,881mil, which is located Zhangjiang HiTech

Park, better known as Silicon Valley of Shanghai. The acquisition was yield

accretive.

Reit in 2013, consisting of the above two properties. In 2015, the Reit

acquired Sandhill Plaza at RMB 1,881mil, which is located Zhangjiang HiTech

Park, better known as Silicon Valley of Shanghai. The acquisition was yield

accretive.

In March 2018, the Reit acquired 98.47% of 6 freehold

commercial real estate in Japan from MJOF, a wholly owned subsidiary of

Mapletree Investments Pte Ltd. The acquisition was also yield accretive and

funded via equity through private placement and debt issuance.

commercial real estate in Japan from MJOF, a wholly owned subsidiary of

Mapletree Investments Pte Ltd. The acquisition was also yield accretive and

funded via equity through private placement and debt issuance.

A year later, protests broke out in Hong Kong after Carrie

Lam introduced the extradition Bill. The bill was then suspended in June but it

did little to restore calm in the city. Finally, in early Sept, she announced a

formal withdrawal of the much-despised extradition Bill. However, it was too

little too late, as protestors are calling for ‘five key demands, not one

less’.

Lam introduced the extradition Bill. The bill was then suspended in June but it

did little to restore calm in the city. Finally, in early Sept, she announced a

formal withdrawal of the much-despised extradition Bill. However, it was too

little too late, as protestors are calling for ‘five key demands, not one

less’.

On the 13th Nov, a peaceful gathering of

protestors turned violent in the Festival Walk and they broke glass and

ceiling, and set fire on Christmas tree. The building was closed for repair and

reopened on 16th January, while its commercial office was reopened

on 26 November. It was a very unfortunate that of all the shopping centre, the

protestors chose to storm into the suburban shopping Mall in Kowloon Tong.

Rents were not collected during the major recovery and repair works till its

official opening.

protestors turned violent in the Festival Walk and they broke glass and

ceiling, and set fire on Christmas tree. The building was closed for repair and

reopened on 16th January, while its commercial office was reopened

on 26 November. It was a very unfortunate that of all the shopping centre, the

protestors chose to storm into the suburban shopping Mall in Kowloon Tong.

Rents were not collected during the major recovery and repair works till its

official opening.

On 4th Dec, its sponsor, injected 2 more freehold

yield accretive properties into MNAC Trust to reduce asset and income

concentration in Hong Kong. The manger has also kindly waived the acquisition

fee. It was seen as a positive move as it is yield accretive and improves its

overall Weighed Asset Lease Expiry (WALE).

yield accretive properties into MNAC Trust to reduce asset and income

concentration in Hong Kong. The manger has also kindly waived the acquisition

fee. It was seen as a positive move as it is yield accretive and improves its

overall Weighed Asset Lease Expiry (WALE).

A few weeks after its opening come the Corona Virus, and

Hong Kong was officially hit by a double whammy of protests and Corona Virus outbreak. The

current situation not only affects Festival Walk but across its portfolio in

Japan and China.

Hong Kong was officially hit by a double whammy of protests and Corona Virus outbreak. The

current situation not only affects Festival Walk but across its portfolio in

Japan and China.

So what should investors do

with their investment under current situations?

with their investment under current situations?

Festival Walk mainly serves the

day to day residents of Kowloon Tong and has been a very resilient mall that

has withstand crisis such as SARS and GFC with growing Net Property Income (NPI)

during such times. It is less dependent on tourist trade like Times Square, Landmark,

Elements, Harbourcity. While operations in FW remains challenging, its NPI may

not be much impacted by the gloomy outlook of tourism in HK hence a direct

comparison in earnings with such properties may not be useful in forecasting

it’s impact on FW’s future NPI.

day to day residents of Kowloon Tong and has been a very resilient mall that

has withstand crisis such as SARS and GFC with growing Net Property Income (NPI)

during such times. It is less dependent on tourist trade like Times Square, Landmark,

Elements, Harbourcity. While operations in FW remains challenging, its NPI may

not be much impacted by the gloomy outlook of tourism in HK hence a direct

comparison in earnings with such properties may not be useful in forecasting

it’s impact on FW’s future NPI.

My view is that the closure of

Festival Walk is just one off and it’s just so unfortunate that of all malls,

the protestors decided to protest in Festival Walk to mourn the death of a

protestor and vandalized the building causing extensive damage that it has to

be closed till January 2020.

Festival Walk is just one off and it’s just so unfortunate that of all malls,

the protestors decided to protest in Festival Walk to mourn the death of a

protestor and vandalized the building causing extensive damage that it has to

be closed till January 2020.

Unfortunately, I was not able to

calculate it’s Passing Rent to calculate the NPI (except Gateway Plaza) unlike how I analysed Champion

Reit in the past because the figures are not released in annual report or

quarterly report except in the IPO Prospectus. I emailed the management to

enquire about Festival Walk’s passing rent, but she seemed to suggest that the rent varies much between

the different trade type. After some calculation, it’s NPI Yield is pretty

stable at 80%, dipping to 75% during times like this, hence it’s possible to do

some future projection of FW’s DPU if the ratio of NPI to distributable income

is stable over the years, including the current FY 20/21.

calculate it’s Passing Rent to calculate the NPI (except Gateway Plaza) unlike how I analysed Champion

Reit in the past because the figures are not released in annual report or

quarterly report except in the IPO Prospectus. I emailed the management to

enquire about Festival Walk’s passing rent, but she seemed to suggest that the rent varies much between

the different trade type. After some calculation, it’s NPI Yield is pretty

stable at 80%, dipping to 75% during times like this, hence it’s possible to do

some future projection of FW’s DPU if the ratio of NPI to distributable income

is stable over the years, including the current FY 20/21.

I like analysing Reits with less

profile of properties because it makes it easy to segment each property group

to analyse it’s earnings. We will begin by looking at the overall numbers and

start with Japan Properties, followed by the two properties in China and FW.

Our focus here is about its earnings rather than the asset valuation. My only concern

on property valuation is its revaluation loss affects the gearing, hence I will

touch on this abit as well.

profile of properties because it makes it easy to segment each property group

to analyse it’s earnings. We will begin by looking at the overall numbers and

start with Japan Properties, followed by the two properties in China and FW.

Our focus here is about its earnings rather than the asset valuation. My only concern

on property valuation is its revaluation loss affects the gearing, hence I will

touch on this abit as well.

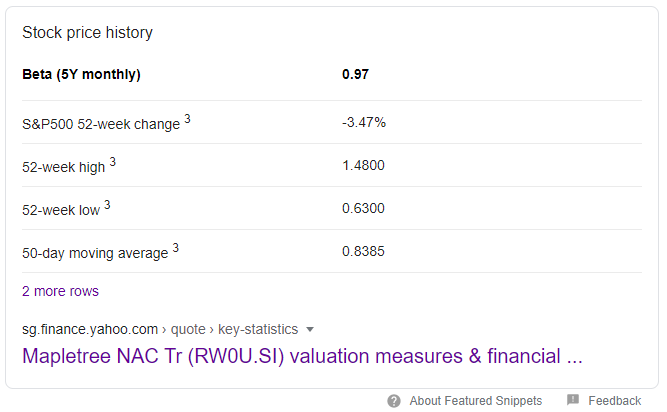

2. Determine the Discount Rate via CAPM

We will be using the

CAPM model to determine the discount rate in this case.

CAPM model to determine the discount rate in this case.

Discount Rate= E(R)= Rf + β (Rm – Rf )

β= 0.97

Rf = 0.884%

Rm= 5.34

Discount Rate= E(R)= Rf + β (Rm – Rf )

= 0.884 + 0.96 (5.34-0.884)

=5.21%

3. Determining NPI Margin

By dividing NPI/ Gross Revenue we

get Net Property Income Margin.

get Net Property Income Margin.

The HK Protest started in June

2019 and then come the Covid 19 this year so the 2Q 2019 onwards its financials

would be in distress. So let’s dive in to the last 3 quarters. June-Sept (2Q), Oct-

Dec (3Q), Jan- Mar (4Q)

2019 and then come the Covid 19 this year so the 2Q 2019 onwards its financials

would be in distress. So let’s dive in to the last 3 quarters. June-Sept (2Q), Oct-

Dec (3Q), Jan- Mar (4Q)

It’s NPI Margin fluctuated between

70% to 80% range, hence its more accurate to assess NPI margin of geographical breakdown

or segment revenue, since the NPI of each segment is provided in the quarterly

earnings report.

70% to 80% range, hence its more accurate to assess NPI margin of geographical breakdown

or segment revenue, since the NPI of each segment is provided in the quarterly

earnings report.

4. Derive the ratio of NPI to Distributable Income to Shareholders

The ratio is fairly stable at low

70% range, from 2015 to 2018, with the exception of 2019, where ratio was 82%.

If we remove the distribution top up, the ratio would be 70.28%.

70% range, from 2015 to 2018, with the exception of 2019, where ratio was 82%.

If we remove the distribution top up, the ratio would be 70.28%.

Hence for this exercise, we can

use a 5 year average.

use a 5 year average.

For simplicity lets use

0.72

0.72

Japan Properties

I will split to 2 sections:

Properties acquired in 2018 & Properties Acquired in 2019.

Properties acquired in 2018 & Properties Acquired in 2019.

5. Analysis of Japan Properties Acquired in 2018

Of the six properties acquired, four

are single tenanted.

are single tenanted.

While there’s tenant concentration

risks in each of the four buildings, I tend to see it positively since these

tenants have undergone a few financial crises in the past and have been

occupying the building since it was built. Relocating office is not an

overnight decision and some single tenanted offices may have purpose-built

facility for its daily operations. Despite Japan’s economy being affected by

Covid-19, I still expect the properties to achieve 100% occupancy or close to

full occupancy.

risks in each of the four buildings, I tend to see it positively since these

tenants have undergone a few financial crises in the past and have been

occupying the building since it was built. Relocating office is not an

overnight decision and some single tenanted offices may have purpose-built

facility for its daily operations. Despite Japan’s economy being affected by

Covid-19, I still expect the properties to achieve 100% occupancy or close to

full occupancy.

Furthermore, all four tenants have good credit ratings and three of four are three of the four single tenants are listed companies and I doubt they

will be defaulting their rent in such a time as this.

will be defaulting their rent in such a time as this.

Moreover, the properties have long

WALE, and with 75% expiring in 2024/2025. 2024 is still sometime away and the

covid-19 would have fade off. Hence, leasing risks is minimal for the next three

years when economy is uncertain.

WALE, and with 75% expiring in 2024/2025. 2024 is still sometime away and the

covid-19 would have fade off. Hence, leasing risks is minimal for the next three

years when economy is uncertain.

To project total distributions coming

from these freehold properties, we assume a zero-growth rate from 2020 to 2024

and a 2% perpetual growth rate.

from these freehold properties, we assume a zero-growth rate from 2020 to 2024

and a 2% perpetual growth rate.

NPI (Japan Properties) for FY

2019/2020= S$39.937mil.

2019/2020= S$39.937mil.

NPI (Japan Properties acquired in

2019)= S$1.8mil (derived from calculation in

2019)= S$1.8mil (derived from calculation in

NPI (6 Japan Properties) = S$39.937mil-

S$1.8mil = S$38.137 mil.

S$1.8mil = S$38.137 mil.

Distributable income per unit from

6 Japanese Properties= (NPI of six Japan Properties* 0.72 ratio)/ (Discount

rate * No. of units in issuance)

6 Japanese Properties= (NPI of six Japan Properties* 0.72 ratio)/ (Discount

rate * No. of units in issuance)

Sum of all PV= $797.464.5 mil

Per share Value from six Japan

Properties= $797.464.5 mil/ 3,342,916,300 units

Properties= $797.464.5 mil/ 3,342,916,300 units

S$ 0.23855

6. Analysis of MBP and OPB (Japan Properties Acquired in

Dec 2019)

Dec 2019)

To reduce concentration risks and geopolitical risks, on 4th

Dec, management decided to acquire two more properties in Japan from its

Sponsor Mapletree Investments. This move is DPU accretive, improved its WALE,

and having more freehold properties in the portfolio.

Dec, management decided to acquire two more properties in Japan from its

Sponsor Mapletree Investments. This move is DPU accretive, improved its WALE,

and having more freehold properties in the portfolio.

The two properties started contributing to its NPI from 28th

Feb 2020 for a month with MBP contributing 87.2% of Gross Rental Income and OBP

contributes the remaining 12.8%.

Feb 2020 for a month with MBP contributing 87.2% of Gross Rental Income and OBP

contributes the remaining 12.8%.

The quarterly report doesn’t disclose the NPI contributed

from the two properties, but I managed to get some information from the acquisition

announcement report.

from the two properties, but I managed to get some information from the acquisition

announcement report.

There is no projection on the gross revenue, but I managed

to find the 6 months NPI for the two Japan properties ending Sep 2019.

to find the 6 months NPI for the two Japan properties ending Sep 2019.

Assuming zero growth and one month of contribution of NPI

from mBay Point Makuhari Building & Omori Prime Building, NPI= S$ 10.8 m/6=

1.8mil.

from mBay Point Makuhari Building & Omori Prime Building, NPI= S$ 10.8 m/6=

1.8mil.

If both properties contributed to NPI for the full 3 months,

5.4m/56.9m *100%= 9.5% that’s about right which should be

higher than the relative figure of 6.4% considering significantly lower NPI

from Festival Walk the past three months.

higher than the relative figure of 6.4% considering significantly lower NPI

from Festival Walk the past three months.

MBP

Prior to its acquisition in Dec, the committed occupancy is

84.8% which is above the average vacancy rate of 7.7-9%. One of the catalysts

for this acquisition is for Reit manager to grow its NPI by improving the

vacancy and capture rental reversion. In view of this Covid-19 impact on

economy and comments from the REIT manager (see below), the base case would be

that current occupancy to remain at 84.8%. I won’t expect further reduction in

occupancy as it’s occupancy is already below average and it’s major tenants are

big companies.

84.8% which is above the average vacancy rate of 7.7-9%. One of the catalysts

for this acquisition is for Reit manager to grow its NPI by improving the

vacancy and capture rental reversion. In view of this Covid-19 impact on

economy and comments from the REIT manager (see below), the base case would be

that current occupancy to remain at 84.8%. I won’t expect further reduction in

occupancy as it’s occupancy is already below average and it’s major tenants are

big companies.

MBP currently contributes 87.2% of the Gross Monthly Rental

Top tenants:

- NTT Urban Development, one of the world’s largest

telecommunication companies with market cap in excess of US98billion listed on

Tokyo Stock Exchange. - AEON Group ,with a market cap in excess of US$18 bil, listed

on Tokyo stock exchange.

OPB

According to report, Vacancy rate expected to maintain

low-level between 1.4% to 3.2% from 2019-2023. It was at 100% occupancy prior

to acquisition in Dec.

low-level between 1.4% to 3.2% from 2019-2023. It was at 100% occupancy prior

to acquisition in Dec.

Although it is a multi-tenanted building with smaller sized

companies, the sectors which major tenants are belonging in: Eighting (Video

Games Developer), Isuzu Linex (Transportation & Logistics) and Brillnics

(Information Technology) seemed to be unscathed by the Covid 19 situation. In

fact, IT and Video Gaming firms may even thrive during Coronavirus.

companies, the sectors which major tenants are belonging in: Eighting (Video

Games Developer), Isuzu Linex (Transportation & Logistics) and Brillnics

(Information Technology) seemed to be unscathed by the Covid 19 situation. In

fact, IT and Video Gaming firms may even thrive during Coronavirus.

I also did some

Googling and guess what I saw. – No available space office at the moment

Googling and guess what I saw. – No available space office at the moment

According to APAC office report outlook, gross face rental

growth projected to be -1.1% in 2020 and 2.6% in 2021. If percentage directly

translates to a -1.1% dip in NPI for 2020 and -2.6% dip for 2021, and staying

constant till 2025 and perpetual growth of 2% from 2025 onwards.

growth projected to be -1.1% in 2020 and 2.6% in 2021. If percentage directly

translates to a -1.1% dip in NPI for 2020 and -2.6% dip for 2021, and staying

constant till 2025 and perpetual growth of 2% from 2025 onwards.

Sum of all PV= $422.8749 mil

Per share Value from six Japan

Properties= $422.8749 mil / 3,342,916,300 units

Properties= $422.8749 mil / 3,342,916,300 units

=S$ 0.1264988

7. Properties in China: Analysis on Sandhill Plaza

The latest quarterly report suggested that Sandhill Plaza

benefitted from the current Covid 19 crisis, as cost sensitive tenants are

inclined to shift to decentralized areas.

Moreover, the tenants are mainly TMT- Technology, Media and Telecom,

which are less affected from the current situation.

benefitted from the current Covid 19 crisis, as cost sensitive tenants are

inclined to shift to decentralized areas.

Moreover, the tenants are mainly TMT- Technology, Media and Telecom,

which are less affected from the current situation.

The latest results speak for itself. Although occupancy

dipped slightly, average rental reversion has increased 10%.

dipped slightly, average rental reversion has increased 10%.

While management commented that the performance is expected

to be resilient, there’s not much room left to grow its occupancy as it has already

hit 98%. The only way is to grow its average rent.

After tabulating the NPI over the past 4 years, it’s earnings are not very stellar,

but growing slowly year on year at CAGR of 0.8%. Hence let’s use a perpetuity

model of 0.8%.

to be resilient, there’s not much room left to grow its occupancy as it has already

hit 98%. The only way is to grow its average rent.

After tabulating the NPI over the past 4 years, it’s earnings are not very stellar,

but growing slowly year on year at CAGR of 0.8%. Hence let’s use a perpetuity

model of 0.8%.

CAGR = 0.8%

Using a perpetual CAGR of 0.8%,

Distributable Income for FY 2020/21 = 16,848 * 1.008 = 16.984784

mil.

mil.

Per share Value= 388.22 mil / 3,342,916,300

units = S$0.11613322

units = S$0.11613322

8. Analysis on Gateway Plaza

Similar to Sandhill Plaza’s analysis, I

have done up the table for it’s NPI and distributable income from FY 2015-2019

have done up the table for it’s NPI and distributable income from FY 2015-2019

And management commented:

There is a dip in NPI in 2017 as

there’s a change in Property Tax derived for China. Hence additional property

tax of $5.4mil.

there’s a change in Property Tax derived for China. Hence additional property

tax of $5.4mil.

I wrote to management to enquire on the passing rent and she

replied that the passing rent is in the range of 320-350 RMB per sq/m. After

digging into some past analyst reports, it was also recorded at 320-350 RMB per

sq/m.

replied that the passing rent is in the range of 320-350 RMB per sq/m. After

digging into some past analyst reports, it was also recorded at 320-350 RMB per

sq/m.

Using 320 RMB as passing rent & NLA of 106,456 sqm, Annual

Gross Revenue =320 RMB per sm *106.456 *12 months = RMB 408.791040 mil.

Gross Revenue =320 RMB per sm *106.456 *12 months = RMB 408.791040 mil.

Let’s assume that passing rent stays at 320 and slowly

recovers to 350 by 2023 and occupancy rate increases from 85% to 96% by 2023.

recovers to 350 by 2023 and occupancy rate increases from 85% to 96% by 2023.

SGD 1= RMB 5

Sum of all present value= $$ 915.282 mil

Per share Value= $$ 915.282 mil

/ 3,342,916,300 units =$0.2737975

/ 3,342,916,300 units =$0.2737975

9. Analysis of Festival Walk

I have to be honest that it’s very hard to analyse on this

one. Even as Covid 19 situation improves, Hong Kong may have to brace for more

protests. Even protestors are getting smarter; to maintain social distancing

during protests and standing 1.5m apart. It’s currently double whammy for HK

government, having to face Covid 19 with the protestor’s situation.

one. Even as Covid 19 situation improves, Hong Kong may have to brace for more

protests. Even protestors are getting smarter; to maintain social distancing

during protests and standing 1.5m apart. It’s currently double whammy for HK

government, having to face Covid 19 with the protestor’s situation.

Although the current protests and Covid 19 may exert

pressure on Festival Walk’s rent, there are two ways to see it. First scenario

is that rental and occupancy will drop drastically like Gateway Plaza. Another

scenario is that Festival Walk could still maintain at high 90% occupancy rate

with only slight dip in passing rent. Reason being that Festival is a suburban mall

and serves the residents in Kowloon Tong and its passing rent is lower than

Champion Reit. Hence, tenants may be looking to locate their shops near residential

malls like Kowloon Tong knowing that shopping centre is less tourist dependant

and cheaper rental, driving up overall demand in suburban mall.

pressure on Festival Walk’s rent, there are two ways to see it. First scenario

is that rental and occupancy will drop drastically like Gateway Plaza. Another

scenario is that Festival Walk could still maintain at high 90% occupancy rate

with only slight dip in passing rent. Reason being that Festival is a suburban mall

and serves the residents in Kowloon Tong and its passing rent is lower than

Champion Reit. Hence, tenants may be looking to locate their shops near residential

malls like Kowloon Tong knowing that shopping centre is less tourist dependant

and cheaper rental, driving up overall demand in suburban mall.

Initially I would want to project it’s NPI through passing

rent psf but realized that it would not be accurate as there are rental reliefs

extend throughout the next few months.

rent psf but realized that it would not be accurate as there are rental reliefs

extend throughout the next few months.

I have also written an email to Elizabeth of investor relations

to enquire on the passing rent psf. She replied me within 2 days and mentioned

that rental rates differ among trade types, but yet to give me an answer on the

average passing rent.

to enquire on the passing rent psf. She replied me within 2 days and mentioned

that rental rates differ among trade types, but yet to give me an answer on the

average passing rent.

I did a comparison between Q2-Q4 for FY2019/20 vs FY2018/19

to assess its impact on the NPI. I included the rental topup as I wanted to

remove impact on Festival Walk’s closure as I see it as a one time even and not

a recurring one.

to assess its impact on the NPI. I included the rental topup as I wanted to

remove impact on Festival Walk’s closure as I see it as a one time even and not

a recurring one.

In fact the worst is yet to come,

considering that April 2020’s NPI is not included and there will be more handing

out of rental rebates.

considering that April 2020’s NPI is not included and there will be more handing

out of rental rebates.

I will use Q2-Q4 2019-2020’s result, and project a one time 20%

reduction for 2021 Revenue due to rental reliefs, followed by a 5% increment

from 2022-2025 (based on 2019-2020’s NPI) & 2% growth perpetually. I don’t think

I am being over optimistic here, considering that it will take another 3 years

to go back to FY 2018/2019’s NPI.

reduction for 2021 Revenue due to rental reliefs, followed by a 5% increment

from 2022-2025 (based on 2019-2020’s NPI) & 2% growth perpetually. I don’t think

I am being over optimistic here, considering that it will take another 3 years

to go back to FY 2018/2019’s NPI.

Sum of all present value= $$ 4,510.8379 mil

Per share Value= $$ 4,510 mil

/ ,342,916,300 units =$1.349372

/ ,342,916,300 units =$1.349372

However, many have doubts on it’s earnings after 2047 the year when ‘one country, two systems’, expires. Your guess is as good as mine, but Xi Jinping spoke in 2017 once that the principle of one country, two systems should remain unchanged. In my opinion, the CCP will extend the status of one country two systems, and property owners can extend the lease of ownership subject to a fee.

If the worst case scenario plays out, where Festival Walk will continue to collect earnings up to 2047,

Sum of present value from 2020 to 2047

= $$ 4,510.8379 mil-

2,811.324 mil

2,811.324 mil

= 1,699.513 mil.

Per share Value= 1,699.513 mil / 342,916,300 units= S$0.50839

10. Summing up altogether+ Intrinsic Value

What are your views about MNAC Trust. Do you think it’s worth more compared to current prices?

Thanks for the hard work putting this together. Very informative.

Oh, by the way, i think yr spellcheck needs rework. Spotted a typo in last para of the article.

Hey Reflections, thanks.

Yeah! ok I spotted it!

Will change it now haha

The future of HK is bleak with the non stop protest and violence.

Commercial property prices has been declining as the rich unload them. China is pivoting to Macau, away from HK.

I am vested since 2014 but will not add more.

Hi, thanks for sharing your view. It's sad to see the current situation in HK. I love Hong Kong because of it's vibrant city and people there are very diligent and driven.

Personally, I am still optimistic on Hong Kong in the long run, as long as Hong Kong still have value to China. I believe that China and asia will benefit from a prosperous Hong Kong.

The former HK Chief executives come together to form alliance to restore hong Kong to resolve the crisis. I am optimistic they will do all they can to restore Hong Kong to its former glory.

CH Tung said “Their intention is to harm the common interests of Hongkongers, and push Hong Kong toward the edge of the cliff… [we] will not let you succeed,” Tung said”

Hell of analysing. Interesting work. Thanks for the effort.

You are welcome Cory! I am glad to be of help. Stay safe!

Thanks for the great analysis!

With the lower demand and higher supply for the Beijing office market, as well as long term concerns that companies may consider cutting costs by shifting some of their offices to decentralised areas, do you think it may be a little optimistic to assume increases in both rent and occupancy for your Gateway Plaza projections?

Hi, thanks for taking time to visit my blog.

Yes, I agree that the monthly rent may have slightly been slightly optimistic, since it is located at Chaoyang district , CBD of Beijing. However I have assumed an occupancy rate of 85% yet as of March 2020, its occupancy rate has been 91.5%.

Also its major tenants, are BMW, Bank of China, China Fortune Land Developement (CFLD). These are big companies,and I don't see them shifting due to short term economic uncertainties and they have a reason to have their office in CBD.

Also because its sponsor is Mapletree hence I also believe in management in maintaing high occupancy levels, and maximizing NPI. Their current quarter result didn't disappoint after all.