Last Thursday, I came across an article in Business Times

about UOB issued negative EUR Bonds and it was 2.6X oversubscribed, with order

book of 1 billion EURO.

It doesn’t make any sense to me in first glance. I always

thought that negative bond yield is only something that’s theoretical, like

negative oil prices, but didn’t expect that anyone could possibly be interested

in buying a bond where the investor is guaranteed to receive lesser money the

original price when bought and held through maturity. It generated strong

demand and analysts predicted that there will be more to come for Singapore

banks. Today, the total negative-yielding debt amounts to USD 17.05 trillion.

It is almost equivalent to the total market cap of Nasdaq, which stand at USD 17.2 trillion as

of Nov 2020!

So I was curious on why are there so much demand in negative

bond yield? Hence, I did some research and discovered some of the reasons why investors would subscribe to such bonds.

As a means of currency hedging

A 7 year- bond yielding at-0.21% may not be attractive for

Singaporean investors holding Sing Dollars. However, investors who are holding onto US

dollars can benefit from a higher yield as compared to US treasuries. Here’s how:

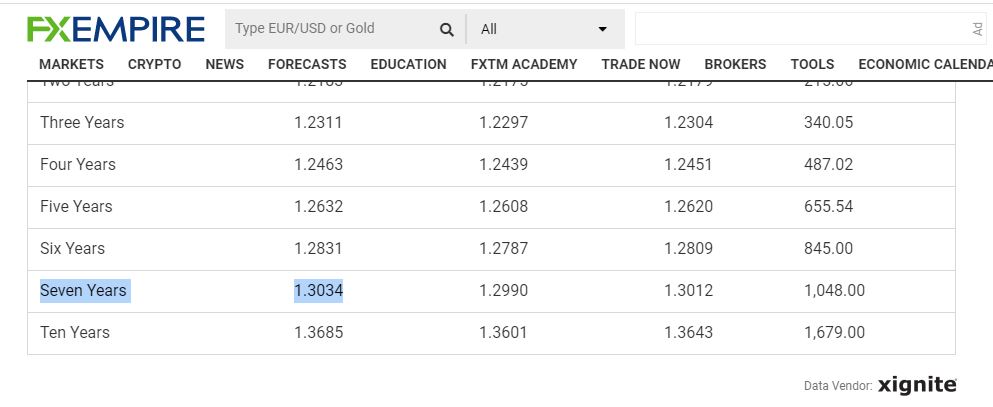

As of 27th Nov 2020, a 7 year Treasury rate

yields 0.61%.

Under normal circumstances, one who invests in X US Dollars in

US treasury at par value will receive USD 1.0435X in 7 years time.

If one converts X USD to EUR, at a rate of 1 USD

= 0.835866 EUR

and then purchase UOB covered Bonds above par of EUR 1.01553 and hold till maturity, he will receive EUR 0.835866X/1.01553.

After converting back to USD based on EURUSD 7-year forward

rate of 1.3034, the final value would be 0.835866X * 1.3034/1.01553= 1.07280x.

The effective yield would be 1.01% can be calculated by

The effective yield would be 1.01% can be calculated byannualizing and it seems more attractive compared to buying 7 Year Treasury

yield which only gives an annualized return of 0.61%.

Capital Gain

In some cases, investors do not intend to hold the bond till maturity. During the course of their holding period, they may benefit from

the sale of negative bond yield if interest rates continue its decline. This is

because of the inversely proportional relationship between bond price and

interest rate/bond yield.

The inverse relationship makes sense if we consider the

example of a zero coupon bond of a treasury bill for simplicity sake. As its

name suggests, zero coupon bond does not pay interest but is issued at a

discount and redeemed at par value.

Suppose a zero coupon bond is yielding 5% and interest rates

were to rise the following day, the newly issued bonds will be sold at a

higher yield and rendering the 5% bond to be less attractive. Hence to attract

demand, the 5% bond has to be sold at a lower price to match the same return

yielded by current interest rates.

If the interest rate declines during the course of holding a negative yield bond, the investor can potentially sell the bond and achieve a positive returns. Hence, negative yield are not correlated to negative returns but do note that it cut both ways. A rising interest rates could erode the investment returns.

For instance, S&P Germany Soveriegn Bond Index.

|

| Bond fund with negative Yield to maturity |

|

| Chart showing positive returns for a German Bond Fund |

In most cases, newly issued bonds tend to have yield that

exceeds or at least match the current national interest rates.

In UOB’s negative bond’s case, a similar comparison would be

Germany’s Bund, due to the similarity in currency, both denominated in EURO and

similar credit rating of AAA by S&P.

-0.714% vs -0.21%

Looking at Germany’s 7 years bond yield just goes to show why UOB’s bond is so well received by investors.

Hedge against deflation

During times of deflation, bonds retain its value well and investors

could achieve a positive return by holding on a negative bond. This happens

when the bond yield is higher than the rate of inflation

The formula for real rate of return is

(1+nominal rate)/(1+inflation rate) – 1 or a more simpler way

to put it

is Nominal rate – Rate of Inflation

A deflation happens when price levels in the economy goes

down as compared to inflation where too much money chasing too few goods.

If I earn a 3% nominal return and inflation stands at 2%, my money is only growing at 1%.

Instead if we have a deflation of 2%, then my wealth is growing at 5%

So investors who expect price of goods to fall may consider investing in a negative yield bonds. With a deflation of -2%, the UOB negative yielding bond may still bring about positive real return.

Based on https://www.macrotrends.net/countries/SGP/singapore/inflation-rate-cpi,

the inflation in Singapore has stayed low and experienced a deflation in 2015

and 2016 as compared to countries like Japan, which has struggled with

deflation since 1990s and bonds has been a useful hedging tool against

deflation. Also the nature of Japan’s yield curve allows investors to make

capital gains through ‘roll down’ method, which essentially means buying and

holding a bond and sell it to enjoy capital gain before it matures. The best

time to take advantage of a roll down is during a low interest environment, yet

with interest rate is expected to rise.

So here are the three reasons why it can be profitable to

invest in negative yield bonds. Now if you are convinced, I am pleased to announce

that I will be issuing SGD negative yield bond, called EOTS Bond. The initial

subscription price is just $100,000, and at the end of the 5 years I will pay

you back $90,000. Limited tranche available, and only on a first come first

serve basis. Please drop me a comment below if you are interested to subscribe.

😊

Thanks for checking out my posts. If you are keen to follow my posts or get updates, please like & follow my FB page here where I will update it when there’s a new post.

The EOTS bond sale is just a joke. I don't want to be called up by MAS to 'lim kopi' 😀

wont you lose your return with all these currency conversion ?

Depends on the provider. Just like buying shares, too high brokerage fees can also erode your total returns.

In any case the negative yield bond is attractive if you compare to German bund.