With Nasdaq trading at its all time high, there’s not much low hanging fruits left and I have to look elsewhere for more unfamiliar tech companies and came to know Crowdstrike Holdings. It is not exactly trading at a cheap valuation, with 33.5 times price to sales. On 6 Jul 2020, I bought 10 shares at $109.12 because of I am convinced there are still plenty of growth ahead and it demonstrated a strong ability to secure clients and high retention rate. As a result, the company had a good run, and recently showing some weakness at $100 range, declining from its overbought level. Moving forward, I will be keeing much cash to potentially buy more on dips.

Crowdstrike Business

Crowdstrike is recognized by Gartner as one of a few leaders in endpoint security . Unlike antivirus (AV) protection where it protects an indivdual personal computer or a device, endpoint security detects malicious activities and protects the whole network including servers and devices from a malware attack. It is more frequently used in enterprises and organizations rather than individual or home use. New corporate cultures such as working from home and bring your own device policies in light of the current situation has made endpoint security more relevant than ever. In fact, Crowdstrike has gotten a boost from Covid 19.

Another difference between a traditional AV and Crowdstrike’s endpoint security is that the former blocks the intrusion of virus or malware by relying on its signature. Hence if the malware was not captured in it’s antivirus database or a software experiences a zero day attack, it could end up firing blanks or left undetected. The latter is cloud based and uses machine learning, realtime monitoring of events to diagnose if a particular file or application is malicious. If it detects a suspicious application, it uploads the particular file to cloud, sandbox it and monitor it realtime for any malicious activities. Hence Crowdstrike is benefitting from sort of a ‘network effect’: the more clients they acquire, the more signals it gets which results in a better threat graph.

Financials

At first glance, it appears that Crowdstrike has relatively high debt. Yet a huge poportion of debt is made up of deferred revenue, which is a plus point to me. Deferred revenue is an unearned revenue Crowdstrike received in advance which its service has yet to be delivered. It is very common in SaaS companies, when a year of subsciption fees are billed upfront. Once delivered, it will be poportionally recognized and show up in income statement under Revenue.

|

| Strong Growth in Deferred Revenue |

A strong growth Deferred Revenue shows that they have managed to secure new contracts which will be delivered during contractual period. Hence, we should keep an eye on its deferred revenue as any signs of slowing deferred revenue will point to a weak sales growth in the next few quarters.

Valuation

Since Crowdstrike is not profitable yet, there are not much valuation metrics which I can apply to this stock. I will be analysing its free cashflow from Q4 2019 to Q1 2021.

As the revenue grows, so does the Net Cash Provided by Operating Activities, with exception of Q1 2020 and Q2 2020. I digged deeper into the financial report to analyze what could have caused a negative operational cashflow in Q2 2020. That quarter showed an exceptionally high General & Administrative Expenses yet there is no explanation on the sudden spike in G&A; but management expects G&A to decrease as a percentage of revenue over time. It could be that G&A expenses incurred in Q1 2020 were only registered in Q2 2020 as Q1 shown relatively low G&A.

|

| Percentage of G&A by Total Revenue |

I plotted the percentage of G&A by GAAP total Revenue and the results seemed to align with management’s anticipation. Hence, it would be fair to assume that the spike in G&A is just a one time off.

The past few years has seen strong revenue growth but management’s revenue guidance for FY 2021 of USD 723-733mil i.e. 53% increase, meant growth will be slower than the prior years.

To value the stock, I will be using a discounted cashflow by extrapolating its growth and then poject its relation to free cashflow through the Free Cashflow Margin.

Using CAPM to calculate Discount Rate:

E(R)= Rf + β (Rm –

Rf )

= 0.69+ 0.91 (5.5)

=5.695

According to MarketWatch.com, CrowdStrike has a beta of 0.91, and that gives a discount factor of only 5.695%. I am a little hesitant to adopt a low discount factor for this growth stock and revise it to 8%.

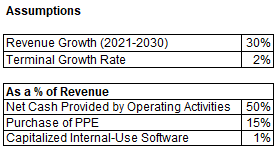

Revenue Growth and Terminal Growth Rate

As Revenue are still growing at high figures, I think that average growth of 30% for the next ten years is conservative for Crowdstrike’s growth.

DCF has two major components: forecast period and Terminal Value. As forecasting gets more challenging when time horizon grows longer, a perpetuity growth rate of 2% is assigned with the assumption that revenue will continue to grow, albeit at a slower pace.

Net Cash Provided by Operating Activities as a % of Revenue

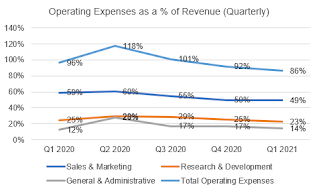

Cash Generated by Operating Activities making up 50% of revenue may seem to be on a high side when Form 10K showed Crowdstrike generating positive cash flow from Operations in Year 2020 with only 21% of Revenue. If we analyze its quarterly reports, cash generated from Operating Activities only started turning positive in 3Q 2020, making up of 31% of Revenue in 3Q 2020 and 43% at 4Q 2020. Hence its net cash generated as a percentage of Revenue in 2020 was actually marred by first two quarters of negative cashflow. It continued to grow with 1Q 2021, making up 55% of Revenue. Currently, Crowdstrike is in its growth stage and its emphasis is on acquiring clients instead rather than profitability and ability to generate cash. Over time, costs as a percentage of revenue could decrease once they have captured a larger share of the market and lesser costs is required to retain existing clients. (see below)

|

| Operating Expenses as a Percentage of Revenue (quarterly) decreases with time |

|

| Operating Expenses as a Percentage of Revenue (Yearly) decreases with time |

Purchase of PPE

Past three quarters’ average was 13% and I would assume a 15% for 2021 onwards.

Capitalized Internal-Use Software

The yearly trend showed a modest increase in Capitalized Internal-Use Software and only comprised of 1% of the Total Revenue for the last two quarters.

Summing up present values= USD 143.28

Potential upside of 43%. (current share price of $100.03).

Whats your take on Crowdstrike Holdings. Would you purchase at current levels?

p/s Indeed its hard to swallow at today’s price to sales of 33.5 times, but such levels simply indicates that market expects strong growth in upcoming earnings. If the upcoming financial results can exceed these demanding valuations, it can still be undervalued.

Anyways, I hope you find this analysis useful or as a starting point to do research on this stock. If there is any particular stock that you would like me to analyse, feel free to drop a comment down below! 🙂

Thanks again for reading. Happy investing and if you are keen to follow my posts or get updates, do like/follow my FB page

here where I will update once there’s a new post.

My Transactions

I am vested at much lower price, hope it really go to 143.

Interesting! I have little knowledge on tech, would say growth investing takes more analysis and guts

Hi,

Wow! good for you. I only came to know this stock when it was at its 80+ range, hesitated abit and only pulled the trigger earlier this month after doing some read up on this company.

All the best to you and yes, looking forward to more price upside!

Hi Mr Llama,

Thanks for dropping by! Read your blog on Lendlease as well, a stock I have invested since IPO for dividends.

For Tech stocks especially those listed on Nasdaq, got to be familiar with the way they present their financial statements, understanding GAAP and non-GAAP reporting.

Will get use to it as you read more. Yes need more guts too but it can be rewarding.

All the best!

The traditional anti virus companies have cloud component where it provides signatures and machine learning as well. The question is more of an implementation, how good it is. that part i am abit detached already.

Hi Kyith! Thanks for dropping by!

Agree with you. Hence, when it comes to investing it such sector, being recognized leader in endpoint security matters alot.

It may face threats from new entrants or even existing companies, hence keeping a close eye on deferred revenue every quarter is important (rather than its revenue).

But so far its ability to retain client is impressive, with 98% gross retention rate and 124% net retention rate, which means the customers got upsold and spend averagely 24% more compared to previous year. This could probably show how good it is (from client's perspective 🙂 )