It’s been 4 months since I update my portfolio. As mentioned in previous portfolio update, I liquidated most of my shares for some property investments which in the end I changed my mind. Hence I have been buying back some of the shares I sold.

Here are my 2 CDP portfolios and another one with StanChart. There’s residual amount of US shares left which I didn’t manage to sell it on time when the bank implemented the min transaction fee. On top of these, I have a POEMS Share Builder and POSB Invest Saver account to do dollar costs averaging which I have been putting in $1,000 and $200 respectively. Moving forward, I am planning to do more passive investing rather than actively managing my portfolio actively because I would like to devote more time at work when I am still in my 20s. (ok, late 20s) Because being young is really an advantage and a resource- in workforce or even in investing and I would like to utilize my strengths to succeed before I turn old. In investing, younger people tend to be able to take on more risks and even compound interest takes time. Whereas the advantage of being young at work is having more energy, more efficient and flexibility.

I must admit that age is catching up. Gone are the university days being able to survive with those 5 hours of sleep for 7 days in a row and mugging for exams and blog in the middle of the night.Today, I need at least 6.5 hours to feel refreshed.

p/s I took a day off from work after my dental appt to rest and update my blog.

|

| My Favourite quote: Feel the fear and do it anyway |

Below are my my investment portfolio.

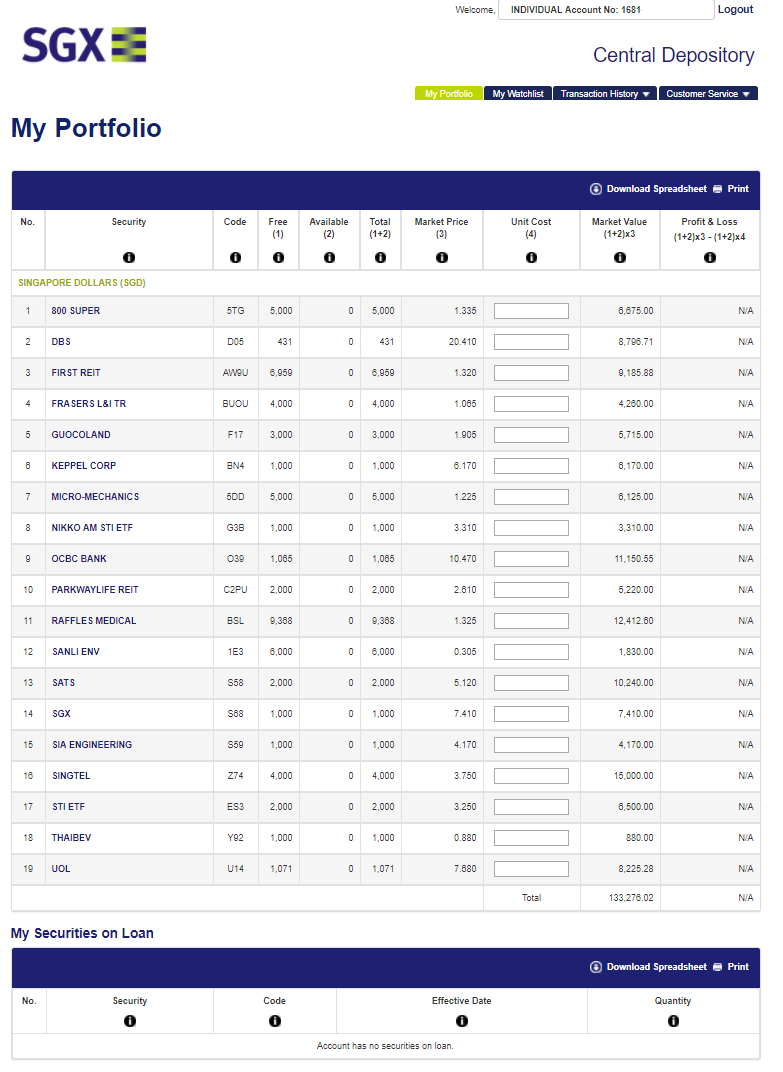

CDP

StanChart

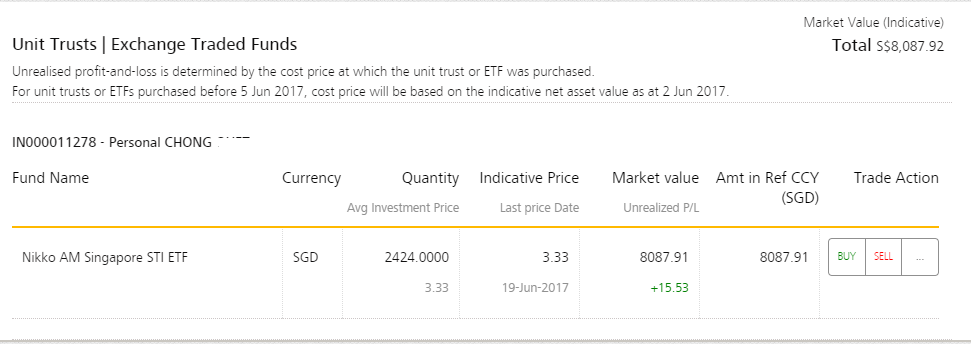

POEMS ShareBuilder

POSB InvestSaver

Cash available for investment

Total portfolio value (inc.cash)= $322k.

Shown below are the shares transacted since last year Sept. I have subscribed to all the scripts dividends including the recent DBS priced at $20.39. The script is not attractive at all but I decide to hold for the long term so I think it will do just fine.

Fraser Logistics & Industrial Trust

I liked the fact that the majority of its properties are (1) freehold, compared to most industrial Reits having short leasehold of below 40 years. Also it has a yearly rental escalation and long weighted average lease to expiry. My preferred choice is still Mapletree Industrial Trust, due to its low gearing and reputable sponsor – Mapletree Investments Pte Ltd but it ran up quite a bit already. It was listed few months before I ORDed and since then it has good track record of growing it’s dividends even during challenging times.

First REIT

I bought back 5000 shares and will add the rest if it falls below $1.30. Recently the stock price experienced a minor dip after the news about the resignation of the CEO and director Dr. Ronnie Tan. Currently, I am waiting to see next quarter’s performance before deciding on adding more. With current CEO Victor’s Tan,who is previous CFO and 9 years of experience at Bowsprit, I am confident that many things are set in place to prepare for this succession plan. Dr. Ronnie also announced his resignation in Auric Pacific Group as a Non-independant non-Executive Director and a member of Audit and Risk Committee in 2016. It seems he is set for retirement unlike Singpost where you see a sudden resignation of CEO, COO and CFO.

Dr Ronnie Tan retires in Auric Pacific:

http://infopub.sgx.com/FileOpen/APGL_Changes%20to%20Board%20and%20Committees_010316.ashx?App=Announcement&FileID=392123

SATS

After selling the shares last year, it went up to a high of $5.30 before it retraced to a range of $4.70 to $5. I took the opportunity to buy during the correction at $4.76 and $4.92. I decided to hold Sats shares for the long term as I liked their management. In the annual report, the Chairman mentioned that they will keep costs low through investing in technology and automation, and he actually kept his words. In the following earnings report, the result speaks for itself. They managed to grow their profit and their FCF through enhancing productivity and costs cutting despite the challenging economic environment.

Here is just one of the examples where Sats invested in automated production line to enhance it’s productivity. Click here for the link

Furthermore, I believe that SATS will benefit from the future construction of Terminal 5, which is 10 times bigger than Singapore’s largest shopping mall or Terminal One, Terminal Two and Terminal 3 combined.

I have actually blogged on SATS 2 years ago. You can read it here.

Starhub

I added Starhub at $2.98 for its yearly dividends of 20 cents/share yielding 6.7% .I bought it few days before the quarterly report hoping for a better set of results to drive up the share prices. Yet, the result wasn’t a good one and unexpectedly announced of dividend cut to $0.16/year, i.e 5.7% yield. I decided to cut loss and move on.

Sanli

After many IPO failed attempts, I was lucky this time and was allotted 6000 shares of Sanli. There are many reasons that I liked this company and I am intending to add more if it drops further. Firstly, it derives 99% of it’s revenue from PUB which is a reputable and credible client. While it may face some ‘concentration risk’ by being over reliant on PUB, the plans to expand their business into southeast Asia region would help to diversify the revenue streams. It also has strong financials: growing profits, increasing FCF and minimal debt. When it comes to management, the founder and executive directors are engineers with experience in this industry ranging from 15 to 20 years. During placement exercise, Heliconia Capital Management Pte Ltd, wholly owned by Temasek, increased it’s shareholding from 6.65% to 7.97% which shows strong institutional support.

Next up, is the share under my watchlist and literally just got filled.(an hour ago)

ComfortDelgro

Today, taxis in Singapore are facing much competition from Uber and Grab. Moreover, these startup companies are giving out with many weekly promo codes that one can end up getting free rides to get from one place to another. Some taxi drivers even made a switch to become grab/uber drivers.

|

| Attractive Grab Promotion |

I always thought that ComfortDelgro derives its revenue from taxi business alone, hence I never took a glance at it when it drop to it’s low earlier this year. Until I read the blog from SG Young Investment. You can read it here. In actual fact, Comfortdelgro has taxi business in 6 different countries also owns 74% of SBS. As of 2016, public transport division accounts for 56.8% of ComfortDelgro’s total revenue. The bus contracting model (BCM) implemented last year has benefited the public transport segment, and it will be paid a service fee and leasing fee in exchange for a fare revenue. As the service revenue is pegged to wage levels, inflation and fuel costs, it’s will bring about stable earnings and won’t get much impacted by external factors such as oil prices or passengers transport demand.

I am also looking forward to the opening of the Downtown Line 3, which will also contribute to its revenue once LTA hands over to SBS.

At 16x pe ratio, I believe it is attractively priced relative to it’s peers such as MTR of HK with 25.1x earnings, and BTS Group Holdings of Thailand at 50.2x. Closer to home, SMRT traded at 23.5x before it got delisted by Temasek Holdings. Hence it’s probably the fact that much pessimism has been factored into the stock price.

Interestingly, my buy order for this stock just got filled as I was writing this blog. Counterparty: MACQUARIE

So how did your stocks and investments perform in June and any thoughts on Comfortdelgro?

Thanks for reading. If you are keen to follow my share transactions, kindly checkout my Facebook page here. I will update my Facebook once my buy/sell order is filled or whenever I wrote a blog post. Selamat Hari Raya Puasa to all my Muslim friends and readers and happy long weekends to all!

Hi you manage to accumulate such big portfolio at around 27 years old. How did you do it? Did you do a lot sideline like tuition?thanks!

Hi Yoyo, personally I don't see it as a big portfolio as many financial bloggers out there already having 500k and above worth of stocks. I am still trying to catch up. Basically I am prudent when saving money and started working before my uni days which sort of gave me a headstart in the workforce.

Hello! Chanced upon your blog from thefinance.sg. you have an impressive portfolio, hope someday I'll have one too.(I just graduated)

I'm just curious of your choice on saving account. Is there any reason to park your cash in UOB wealth account instead of other high interest yielding saving account? Like ocbc 360 or standard chartered bonus$aver?

Cheers!

Hi majulahmillennials,

I applied for a wealth banking account to qualify for the capitavoucher when I deposit fresh funds of 100k. It was back then when I accumulated 100k for the property investment which I changed my mind.

Other than that, there's not much benefits to park in Wealth Banking account.