As we all know, STI has been moving up steadily this year, driven by bank and property counters. Year to date, it’s one of the best performing index in the world. Hence to search for good yield, I have expanded my radar to look beyond just blue chips and the common REITs. Recently, Accordia Golf Trust’s attractive yield caught my attention when it reported its earnings. It is operated in Japan and I don’t have much knowledge on golf business and it’s future prospect. So I did some read up and in this article, I will be focusing more on the outlook on the golf sector in Japan rather than the numbers.

started. In August 2014, Accordia Golf, which owns 133 golf courses, decides to

be asset light and focus more on golf course management. Accordia Golf Asset

LLC was then set up and Accordia Golf transferred 89 golf courses to Accordia

Golf Asset LLC (fully owned by Accordia Golf then). Next, it transferred

this silent partnership stake in Accordia Golf Asset LLC to Accordia Golf Trust

for approx 113bn Yen. This purchase was financed through IPO by listing in SGX, JPY 25.4bn from Accordia Golf (28.85% stake in AGT), and JPY 45.0bn loans.

Manager of AGT, which manages the business trusts and safeguard interests of

investors, jointly owned by Daiwa Real Estate Asset Management Co. Ltd and

Accordia Golf Co Ltd. Currently AGT is granted the first right of refusal over the

sponsor’s golf courses and driving ranges and Daiwa Real Estate Asset

Management Co Ltd provides asset management advice to AGT i.e.

acquisition/disposal of golf course.

summarize the whole picture.

In simple words, Accordia Golf spinned off 89 of its golf course asset by listing AGT to focus on providing golf management services . With Accordia Golf Trust having call options over Accordia’s Golf course and first right of refusal over the courses that Accordia buys or sells, it will be able to acquire golf courses to grow its revenue.

The chart above shows the rise in population

aging with a steady increase in population aged 60s and projected to rise till

2040. On the inverse, there is a fall in population below age 20-59 due to

falling birth rates.

chart below shows a rising trend of percentage of golfers above 50 & 60,

which occupies about more than 50% in 2011. A possible reason may be that golfers at those age group are retired and have more free time to play. With

medical advancement moving forward, life expectancy in Japan is also set to

increase albeit a gradual one.

Entry/ Competitive Advantage

remains high and a typical golf course requires 50-80 hectars, costing about

JPY5 billion to JPY6 billion in construction costs (excluding acquisition price). According to IPO prospectus, there has been no development of new golf

courses partially due to lack of develop-able land, which shows that

competition is limited and is likely that Accordia is able to maintain its market share in Japan.

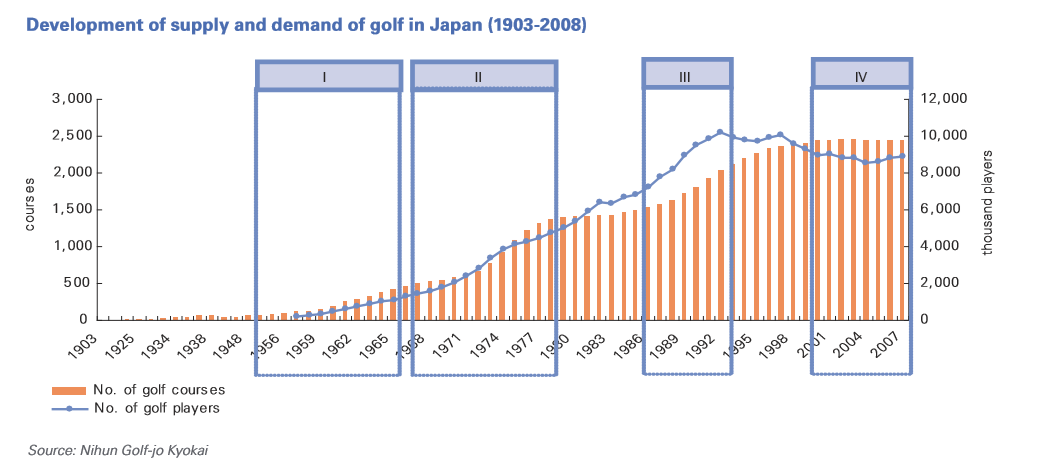

competition makes it harder for new entrants, you have to look back into the

development of the golf industry since the 1900s.

phases.

Phase 1

million golfers and about 500 golf courses in the country. Back then membership

are obtained via shareholder memberships.

Phase 2

very popular sport to entertain clients by mixing business and pleasure. This was when a deposit system was introduced which was to

be paid by a new member and could be fully refunded with no interest should one

terminates the membership.

Phase 3

membership were easily sold with an increased demand. Golf companies

then used the cash for golf development purposes as well as investment products.

With the surge in players, they had never expected that one would consider to

terminate their membership.

where a membership costs up to a few millions

Phase 4

golfers shrank. That was when many golf companies faced pressures from members

to request for refund. Many finally troubled firms couldn’t pay off went into

bankruptcy and some were bought over by Accordia Golf and Pacific Golf

Management (PGM).

Today, it becomes the situation where large size golf companies like Accordia are expanding their market share through acquisitions which smaller companies finds it hard to compete as they are lacking in economies of scale. The smaller golf courses located in more outskirts of city are poorly managed and had to resort into alternative ways to dispose/convert their assets As reported in the IPO prospectus, 37 golf courses have plans to turn their land into solar power plants and the chart below shows the reduction in golf courses after peaking in 2002.

courses in Japan, followed by PGM group. As mentioned, both have acquired much

golf courses since 2000, and specialize in golf courses and driving range

management compared to other companies, who are conglomerates and dealing

with financials, real estate, etc. For instance, OrixGroup, third in line is a

financial services group which owns baseball teams.

Olympic 2020

A possible catalyst to reignite the popularity of golf would be it’s inclusion in 2020 Olympics in Toyko, starting from Rio in 2016. However to stimulate interest in golf and tourism much also depends on the government continuing initiatives and it’s abit hard to forecast the numbers at this point. A question to ask is that would one start playing golf after realizing that his country is hosting Olympics in 2020 with golf being introduced as an Olympic sport? It may create some awareness but I doubt that it would arouse much interest among the younger generation.

I used to think that Olympic Games will boost the the host country’s economy via tourism growth, and was quite bullish on emerging markets like Brazil, as they hosted the World Cup and then Olympic Games 2 years later. However, the analysis report suggest otherwise.

Based on the analysis conducted by McKinsey, host countries for Olympic games sees mixed momentum in tourism growth. Hence, I wouldn’t be too optimistic that Tokyo 2020 would bring much golf tourism to Japan.

it’s profit and distribution:

Internal Growth – growing number of visitors

refusal

visitors)

rewards programme (Jan to Jun 2015) to encourage more players during weekdays. They also implemented the loyalty card programme and as of

March 2016, there are 4.14mil loyalty card holders, which represents 57.5% golf

holders in Japan. Since its launch, there is a steady increase in the

membership. So today, one can imagine that more than half of the golf players

in Japan actually owns a Accordia Golf loyalty card. Having a loyalty card

helps to retain and capture new market share.

economic bubble due to decline in golf visitors, internal expansion will be

limited in the short to medium term. The

below article shows that Japan’s golf courses are closing at a rate of one a

week, due to declining interest among the young and the older generations.

more assets)

of having sponsor is having first right to refusal in purchase of assets. Currently

Accordia Golf has 25 golf courses, and Accordia Golf Trust has call option over

17 of them. As the LTV stands at a conservative 28.8%, there is ample room to

fund acquisition via debt.

administration centre, promoting self-service or installation of automated

payment machines. This means cutting down expenses to improve profit margin and cashflow for distributions. However, it’s hard to read from the report if this actually pays off or whether it’s effective.

Will I buy?

I have given some thought and won’t be purchasing this counter because the earnings are very unpredictable especially with seasonality risks and complicated operating structure. Moreover Japan’s golf population has been declining which seems like a sunset industry. This stock indeed has competitive advantage compared to other golf courses and it has high yield among Reits in Singapore but in this case I am willing to forgo the high yield for something safer. What are your thoughts and would you invest in Accordia?

I like this counter and will continue to grow my position over time and if prices remain stable. Need to factor in potential from the Japan IRs that will sprout and increasing foreign tourists into Japan. Also MBK could be a savvy investor and that could enhance value over time.

Yes I would and more if the prices remai stable and so do the yields.

With the nature of business of accordia golf trust, one has to demand a yield of at least 9%

Hi, thanks for sharing your view. Yes, MBK bought over it's sponsor- Accordia Golf and they mentioned that they will acquire golf courses and improve on it's tourism.

As for the IR bringing in more tourists, I am not too sure if would translate to revenue growth. I have clients who travels to JB to play golf with friends that's because it's cheaper and near to Singapore; But I doubt it's cheap to play golf in Japan. I may be wrong as I am not a golfer and unsure on how are they gonna executive the strategies.

Yup, I am also looking for stable yield

Yup I agree, but I am willing to forgo its high yield for something more stable.

Great insights and good take on AGT.

I am currently holding a small position on this counter and will continue to hold it for the time being.

Thanks Richard for the compliment. Glad you find it useful.

With MBK's recent acquisition of it's sponsor, I hope AGT will do well and take its business to new heights! 🙂

Climate change maybe positive rather than negative for AGT

Why would you think so?